There is a number that most retail traders have never heard, but that now governs a significant portion of what happens to equities every single trading day.

The number is zero.

Specifically: zero days to expiration. And the options contracts that carry that label have quietly become one of the most structurally important forces in modern markets.

Not as a footnote. As a majority.

What 0DTE Actually Means

A zero-days-to-expiration option is exactly what it sounds like: an options contract that will expire at the end of the current trading session. No overnight risk. No waiting. You buy or sell, and by 4:00 PM Eastern, the contract is either worth something or it is worth nothing.

That immediacy is exactly what made them attractive. For speculators, the leverage is extraordinary — small moves in the underlying can produce multiples of return (or total loss) within hours. For hedgers, they offer surgical, single-day protection without the cost of holding options overnight.

For years, 0DTE contracts were a niche tool. Something used by professional options desks. Something that required deep understanding of gamma dynamics and expiry mechanics to deploy safely.

That era is over.

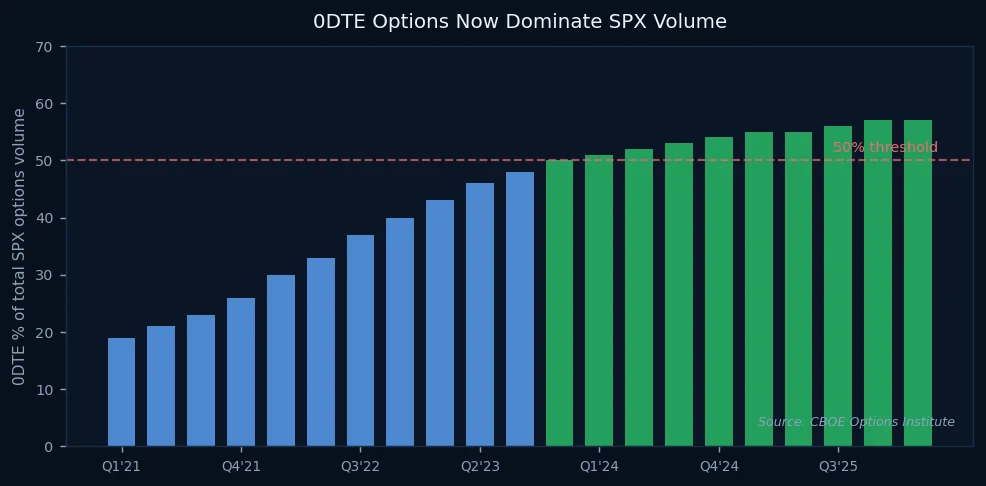

0DTE contracts now represent more than 55% of all SPX options volume — up from roughly 19% in early 2021. In five years, a niche instrument became the dominant mode of options trading on the most liquid index in the world.

And the market has not been the same since.

The Mechanics Nobody Explains

To understand why 0DTE matters to traders who have never touched an options contract, you need to understand gamma.

Gamma measures how quickly an option's delta changes as the underlying moves. As expiration approaches — particularly in the final hours — gamma becomes extremely elevated. Near-the-money options are exquisitely sensitive to every tick.

This creates a mechanical consequence: market makers who sell 0DTE options must hedge aggressively. As price moves toward or away from strike prices, their hedging requirements force them to buy and sell the underlying in increasingly concentrated bursts.

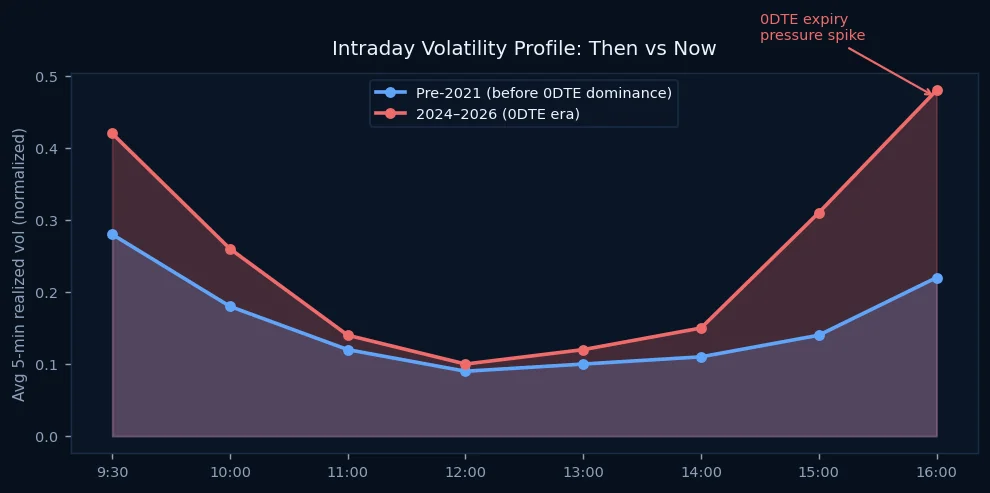

The result is clearly visible in intraday volatility data. The open and close — already elevated periods — have become significantly more volatile in the 0DTE era. Not because sentiment changed. Because the mechanical hedging pressure of hundreds of billions in expiring gamma concentrates into those windows.

This is the invisible hand that systematic traders now have to account for. The 9:30 spike is no longer just institutional positioning and retail reaction. It is, in significant part, a 0DTE hedging cascade.

The Gravity Wells at Round Numbers

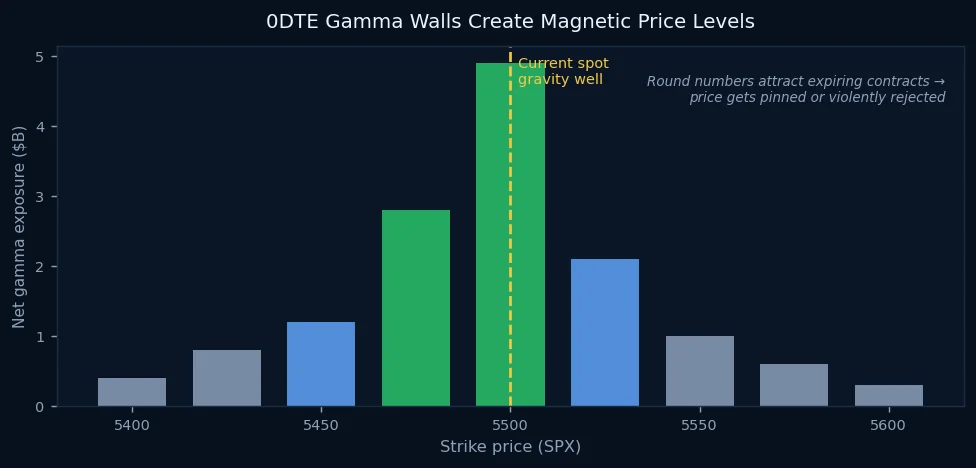

There is another phenomenon that has become increasingly documented: price pinning at round-number strikes.

As 0DTE contracts near expiration, contracts at or near the current price carry maximum gamma. When a large volume of open interest sits at a specific strike, market makers' hedging flows can create a gravitational pull that holds price near that level — or violently repels it once the pin breaks.

The 5500 level is not special because of fundamental valuation. It is special because thousands of 0DTE contracts written at that strike create a mechanical force field. Price approaching 5500 triggers hedging flows that slow momentum. Price breaking away from 5500 releases that pressure in an accelerating burst.

For mean-reversion strategies, this creates identifiable patterns: compression near key strikes, followed by expansion when the pin fails. For trend-following strategies, it creates false dawns — what looks like a breakout is absorbed by gamma hedging until option inventory is cleared.

What This Means for Systematic Traders

The 0DTE revolution has changed the game in ways that reward pattern recognition and punish rigid rule-following.

Old market structure assumptions — smooth intraday trends, predictable volume distribution, consistent volatility across sessions — are increasingly unreliable. The new reality is episodic volatility: compressed and range-bound near large gamma walls, then explosive when those walls are breached.

Algorithmic systems that were tuned before 2021 may now be firing signals into regimes they were never trained to navigate. The morning session in particular has become a different animal. Not worse. But different.

The traders who adapt to this new structure — who understand where the gamma walls sit, when the hedging flows are likely to peak, and why the final thirty minutes of the session have become uniquely violent — will have an increasingly large edge over those who are still fighting 2018's market.

The zero has changed everything. Most people just do not know it yet.