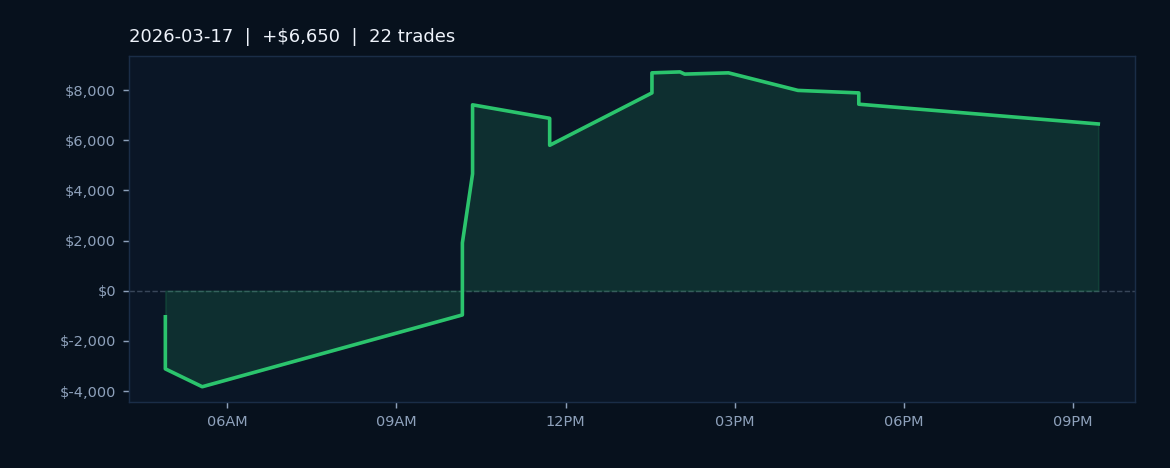

# Market Recap: Tuesday, March 17, 2026

Equity index futures drove trading activity on March 17, 2026, with the platform executing 22 trades across ES (E-mini S&P 500) and MES (Micro E-mini S&P 500) contracts. The session closed with a net gain of $6,650.00, reflecting disciplined risk management across a moderate trading volume. The 45.5% win rate indicated that while roughly four of every nine trades resulted in losses, position sizing and exit protocols effectively contained downside exposure, allowing profitable trades to offset unsuccessful ones.

Volatility characterization during the session suggested a market environment favorable to algorithmic execution, with algorithmic strategies showing consistency in capturing intraday movements within the broad equity index space. The concentration of activity in ES and MES reflected traders' preference for the most liquid large-cap benchmark instruments. With an average P&L per winning trade suggesting meaningful average wins relative to average losses, the session demonstrated the mechanics of positive expectancy in action: selective entries, controlled sizing, and mechanical adherence to exit parameters.

The profitability outcome on March 17 reinforced the value of systematic trade management. While a 45.5% win rate sits below the 50% threshold many traders initially expect, the session's final tally underscored that win percentage alone does not determine trading results. The relationship between average winner size, average loser size, and position sizing determines profitability. The platform's performance that day set a baseline for understanding how subsequent sessions in late March would build or deviate from this pattern of disciplined execution.