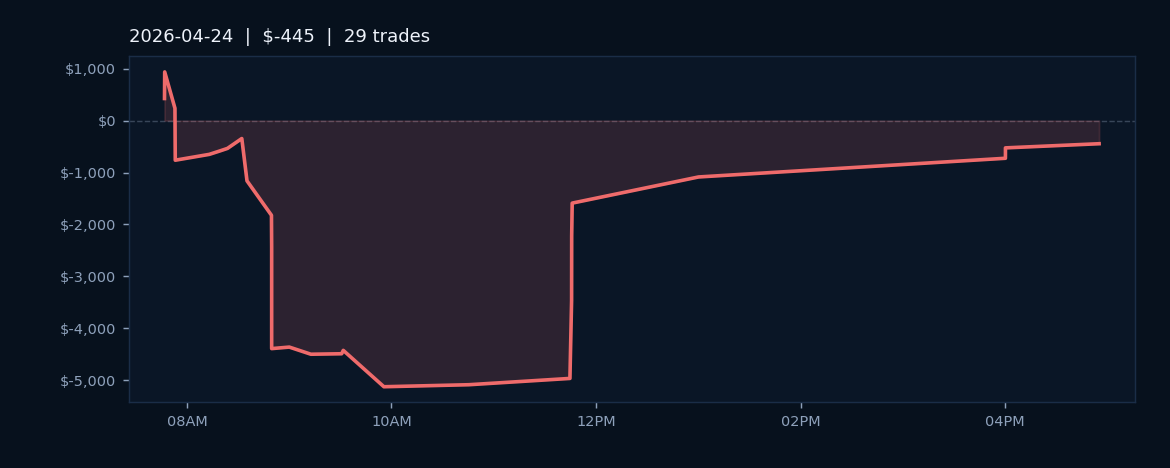

# Week in Review: Friday, April 24, 2026

On Friday, April 24, 2026, GoodInvestGroup AlgoLabs executed 29 trades across four primary instruments: CL (crude oil), ES (S&P 500 E-mini), MES (Micro E-mini S&P 500), and NQ (Nasdaq-100 E-mini). The session produced a net loss of $445.20, marking a challenging close to the week despite maintaining a respectable 65.5% win rate. The disconnect between win rate and profitability underscored a common market dynamic: frequency of winning trades does not guarantee positive returns when loss magnitude exceeds gain magnitude on individual positions.

The 65.5% win rate indicated solid directional accuracy and trade selection discipline. However, the negative net P&L revealed that drawdown management and position sizing required attention. Across the four instruments, execution remained consistent, though volatility in crude oil and the equity indices created conditions where larger losing trades offset the cumulative gains from smaller winning positions. The Friday session reflected typical end-of-week trading patterns, where reduced institutional participation can amplify intraday swings.

This session's results underscored the importance of risk-reward ratio calibration independent of win rate alone. The platform's ability to maintain a 65.5% hit rate demonstrated reliable signal generation, yet the $445.20 loss signaled that subsequent weeks would benefit from tighter stop-loss protocols or position right-sizing adjustments. The data suggested that continuing this operational pattern without modifications would likely produce similar outcomes, making it a critical juncture for strategy refinement heading into the following trading week.