# Market Recap: Wednesday, March 11, 2026

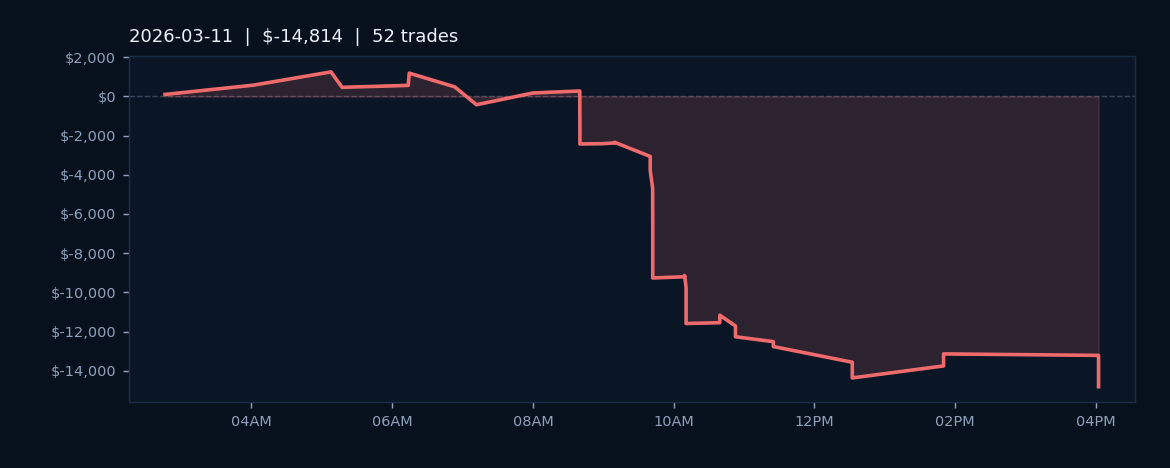

Wednesday, March 11, 2026 proved to be a challenging session for algorithmic trading activity across the S&P 500 futures complex. Across 52 trades executed in ES and MES contracts, the day produced a net loss of $14,813.75, reflecting difficult market conditions or execution headwinds that limited profitability. The win rate settled at 40.4%, indicating that losing trades outpaced winners by a meaningful margin. This outcome suggested that the directional bias or entry signals generated during the session faced resistance, whether from intraday volatility, gap risk, or broader market indecision.

The loss magnitude and win rate combination on March 11 illustrated the inherent risk of algorithmic trading in lower-conviction market environments. With roughly four out of every ten trades finding profitable closure, the risk-reward structure of executed trades appeared unfavorable on that particular day. The reliance on ES and MES exposure meant concentration in a single asset class, which amplified the impact of any adverse price action in large-cap equities.

The session's results underscored that even systematic trading approaches encounter periods of underperformance when market microstructure or macroeconomic conditions diverge from recent patterns. March 11, 2026 joined the historical record as a day when execution discipline and proper position sizing became critical safeguards against drawdown severity. The trading data from this session served as a reminder that subsequent market sessions would need to demonstrate improved entry quality or adjusted risk parameters to restore profitability.