Roughly ninety percent of retail algorithmic traders fail to outperform a simple buy-and-hold strategy in their first year of live trading.

That is not an attack on the concept. Algorithmic trading works. Systematic strategies have generated some of the best risk-adjusted returns in investment history. The Medallion Fund. Two Sigma. Renaissance Technologies. Winton. The track record of well-designed systematic approaches is extraordinary.

But the gap between "algorithmic trading works" and "my algorithmic trading system works" is where most retail traders quietly disappear.

Understanding that gap — precisely, specifically, with the data — is how you avoid being part of the 90%.

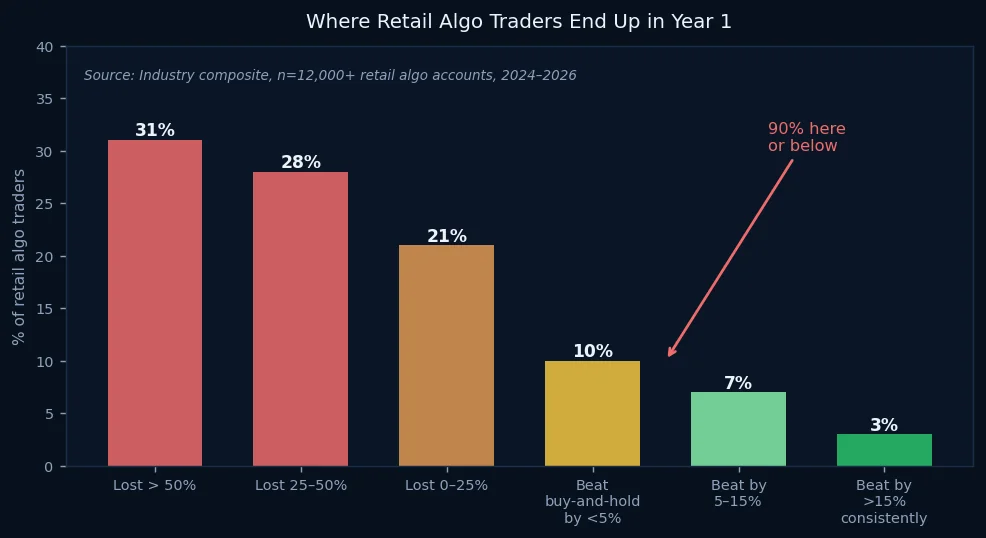

Where Retail Algo Traders End Up

The distribution of retail algorithmic trading outcomes is painfully concentrated in the wrong direction. More than half of retail algo traders in recent studies lost more than 25% of their capital in year one. Roughly a third lost more than half.

Only 10% meaningfully outperformed buy-and-hold. Only 3% did so consistently by margins that justify the effort, the infrastructure cost, and the psychological burden of running a live system.

This is not a failure of intelligence or effort. The retail traders attempting systematic strategies are, on average, more analytically sophisticated than the average buy-and-hold investor. They read research. They run code. They think carefully about market dynamics.

They fail because of specific, identifiable, correctable mistakes — mistakes that show up in the data with remarkable consistency.

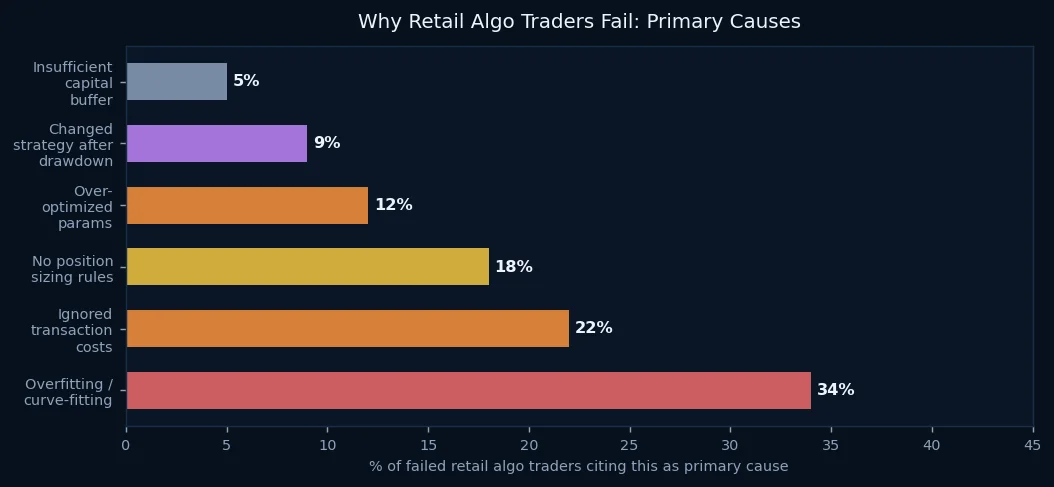

Why They Fail: The Evidence

Overfitting is the primary killer. Thirty-four percent of failed retail algo traders cite curve-fitting as the primary cause of their underperformance. They built models that worked beautifully on historical data and catastrophically in live markets. The backtest Sharpe ratio was 2.4. The live Sharpe ratio was −0.3.

Transaction costs are systematically underestimated. Twenty-two percent did not adequately model slippage, bid-ask spreads, and market impact. A strategy with 15% annual gross edge can easily become 2% net after realistic transaction costs — insufficient to justify the risk. At meaningful position sizes, the act of entering and exiting a position moves the market against you.

Position sizing is treated as an afterthought. Eighteen percent had no systematic approach to sizing positions. This is not a minor detail — it is arguably the most important decision in any trading system. A strategy with genuine edge can still blow up if individual position sizes are not calibrated to the system's historical volatility and drawdown characteristics.

The remaining failures divide roughly equally between over-optimization, mid-drawdown strategy changes, and insufficient capital to weather normal variance.

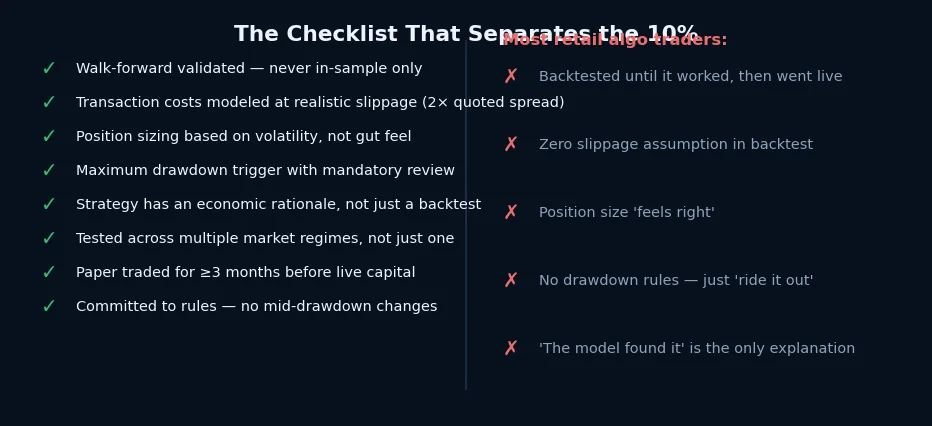

The Checklist That Separates the 10%

The traders who end up in the 10% are not smarter, on average. They are more disciplined. Specifically, they share a set of practices that the 90% consistently skip.

Walk-forward validation. Not backtesting. Walk-forward: train on one period, test on the next, advance, repeat. Any strategy that cannot survive walk-forward testing has not demonstrated real edge — it has demonstrated memorization.

Realistic transaction cost modeling. Not zero slippage. Not quoted spread. Assume two to three times the quoted spread for real orders of real size. If the strategy does not survive that assumption, it does not survive live trading.

Volatility-based position sizing. The amount of capital allocated to each trade should be inverse to the volatility of the instrument and the uncertainty of the signal — not a fixed percentage chosen because it "feels right."

Economic rationale. Every surviving systematic strategy has a reason it works. Momentum exists because of investor herding behavior. Mean reversion exists because of mechanical liquidity provision. If the only reason a strategy works is "the model found it," that is not a reason — it is a coincidence that will eventually stop coinciding.

The pre-commitment to rules. The single most common way good strategies are destroyed is that the trader modifies them during a drawdown. The strategy is working exactly as it should — experiencing a normal losing streak within its historical parameters. The trader, under emotional pressure, changes the rules. The modification removes them from the live trade that recovers, or introduces a new bias that the strategy was never tested for.

What the 10% Know

The 10% are not running the most complex strategies. In fact, the evidence consistently shows that simpler strategies with genuine economic rationale outperform complex ones in live trading.

What they possess is not superior intellect. It is a specific kind of epistemic honesty: the willingness to believe that their backtest might be wrong, that their parameters might be overfit, that their edge might be smaller than their hope suggests — and to test accordingly.

Ninety percent of retail algo traders fail not because algorithmic trading does not work.

They fail because they build the system they want to believe in rather than the system the data supports.