America possesses one of the largest sovereign gold reserves in human history.

Yet on the books of the United States government, that gold is still officially valued at just $42.22 per ounce — a statutory accounting price rooted in the collapse of the Bretton Woods era more than fifty years ago.

This creates a striking disconnect.

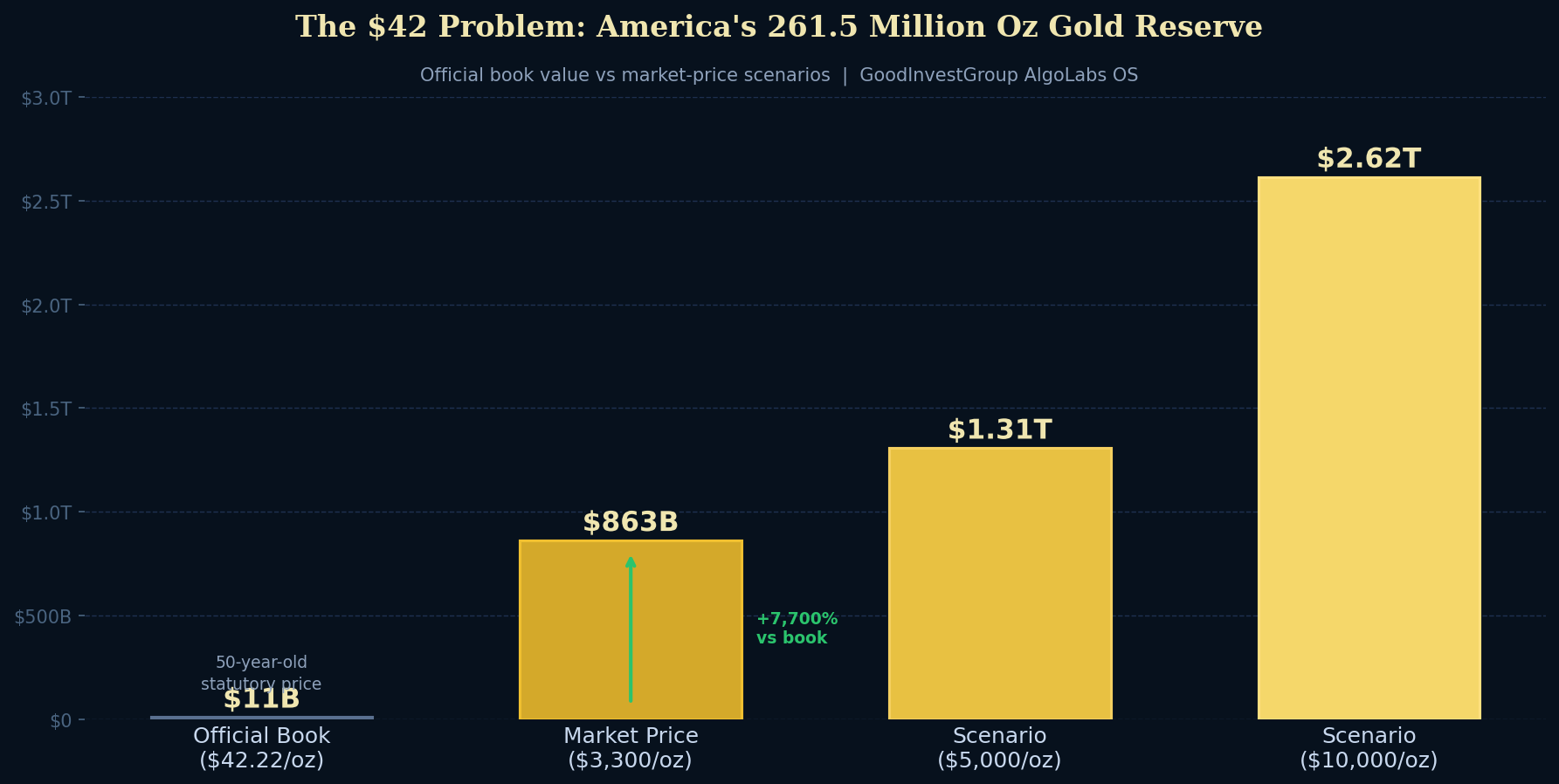

The United States holds roughly 8,133 metric tons of gold, equal to approximately 261.5 million troy ounces, making it the largest official sovereign holder of gold in the world. But despite gold trading at modern market prices measured in the thousands of dollars per ounce, the Treasury continues to value this reserve at a legal price established in another monetary era.

The result is an official book value of only about $11 billion.

This raises an increasingly interesting question:

What if America revalued its gold reserves closer to market value and used the resulting balance-sheet strength to help seed a U.S. sovereign wealth fund?

The idea is controversial.

To supporters, it represents a modern recognition of sovereign assets and an opportunity to convert dormant reserve value into productive national capital.

To critics, it risks becoming accounting theater, fiscal engineering, or even a dangerous form of indirect monetization.

The truth lies somewhere between those extremes.

This is not a proposal to return to the gold standard.

Nor is it a claim that gold can magically erase America's debt burden.

Instead, it is a question about whether the United States is underutilizing a strategic national asset while other nations increasingly think in terms of sovereign capital, long-term investment, and national balance-sheet strategy.

---

America Is the Outlier

Most people assume central banks value gold similarly.

They do not.

The United States is unusual.

The U.S. Treasury values gold at its statutory price of $42.22 per ounce, largely unchanged since the early 1970s.

Many other central banks and monetary authorities, particularly within Europe, use systems that periodically revalue gold near market prices.

Rather than fixing gold at a decades-old legal price, these systems often record changes in gold prices through gold revaluation accounts.

When gold rises in price, the sovereign or central bank balance sheet reflects that increased value — without selling a single ounce.

This means many countries effectively allow gold appreciation to strengthen sovereign financial positions over time.

The United States does not.

This makes America the accounting outlier among major reserve powers.

---

The Math Behind America's Gold

U.S. official gold holdings: 261.5 million ounces

Current legal valuation: $42.22/oz → Book value ≈ $11 billion

Scenario 1 — Market Valuation at $3,300/oz 261.5M × $3,300 ≈ $863 billion (+$852B above book)

Scenario 2 — $5,000 Gold 261.5M × $5,000 ≈ $1.31 trillion (+$1.30T above book)

Scenario 3 — $10,000 Gold 261.5M × $10,000 ≈ $2.62 trillion (+$2.61T above book)

These numbers are not predictions. They are simply valuation exercises demonstrating the scale of sovereign assets already held.

The immediate reaction from critics is predictable: "This is just accounting."

And partly, they are right. But accounting matters. Balance sheets matter. How sovereign assets are recognized matters — and governments routinely make policy decisions based on those realities.

---

Understanding the Treasury–Federal Reserve Mechanics

The gold itself is owned by the U.S. Treasury. The Federal Reserve does not own Fort Knox.

Instead, the Fed holds gold certificates issued by Treasury that reflect the statutory value of Treasury gold holdings — currently reflecting the old $42.22 legal price.

If Congress changed the statutory price or authorized revaluation, several things could occur:

- Treasury's gold assets would rise in recognized value - Gold certificates issued to the Federal Reserve could potentially be adjusted to reflect the new valuation - This could influence Treasury financing flexibility and government balance-sheet positioning

While revaluation itself does not create new physical wealth, it may influence how sovereign wealth is recognized and utilized. That distinction is central.

---

The Sovereign Wealth Fund Question

Many nations already think this way.

Norway transformed petroleum wealth into one of the world's largest sovereign wealth funds. Singapore built sophisticated state investment platforms. Gulf states have used energy assets to create long-duration national capital pools.

The United States, despite being the world's largest economy and issuer of the global reserve currency, has no comparable national sovereign wealth fund of meaningful scale.

Could revalued gold help seed a U.S. National Wealth Fund? Not by selling Fort Knox. Not by nationalizing markets. But by modernizing sovereign accounting and strategically capitalizing long-term investment.

Scenario A2 — $500B Fund compounded at 7%: - 10 years → ~$983B - 20 years → ~$1.93T - 30 years → ~$3.81T

The real power is not the initial seed. It is the compounding over decades.

---

Could This Help National Debt?

Here is where rhetoric often exceeds reality.

America's debt exceeds $36 trillion. Gold revaluation alone does not erase that. Not remotely.

But debt is not only about principal — it is also about servicing cost.

A $500B sovereign fund at 5% generates ~$25B annually. At 7%, ~$35B annually.

Part of that income retained. Part supporting strategic investment. Part offsetting borrowing pressure.

This does not eliminate debt. But it could reduce fiscal strain and create an income-producing sovereign asset. That is a very different conversation.

---

The Risks Are Real

Critics deserve serious consideration.

Market perception risk: If investors conclude Washington is monetizing assets to avoid fiscal discipline, reactions could include higher bond yields, inflation concerns, dollar weakness, and market volatility.

Governance risk: A sovereign wealth fund could become politicized. Who governs it? Who selects investments? Poor governance could turn national investing into political patronage.

Capital markets objection: America already possesses deep capital markets and borrowing flexibility. Supporters must explain why sovereign capital adds value beyond existing tools.

---

The Bigger Question

This debate is ultimately larger than gold.

Gold alone cannot pay America's debt. Nor can it guarantee prosperity.

But it raises an uncomfortable and increasingly relevant question:

Should the United States continue treating one of the world's largest sovereign reserve assets primarily as a historical relic — or consider whether its recognized value could support long-term national investment and capital formation?

The issue is not nostalgia for gold.

It is whether America should think more deliberately about sovereign assets in a century increasingly defined by strategic competition, industrial policy, and national investment.

Perhaps the real debate is not about gold at all.

Perhaps it is about whether America is prepared to think like a nation managing wealth — rather than merely managing liabilities.

---

This analysis is for informational purposes only and does not constitute financial or investment advice.