# Market Recap: Tuesday, April 21, 2026

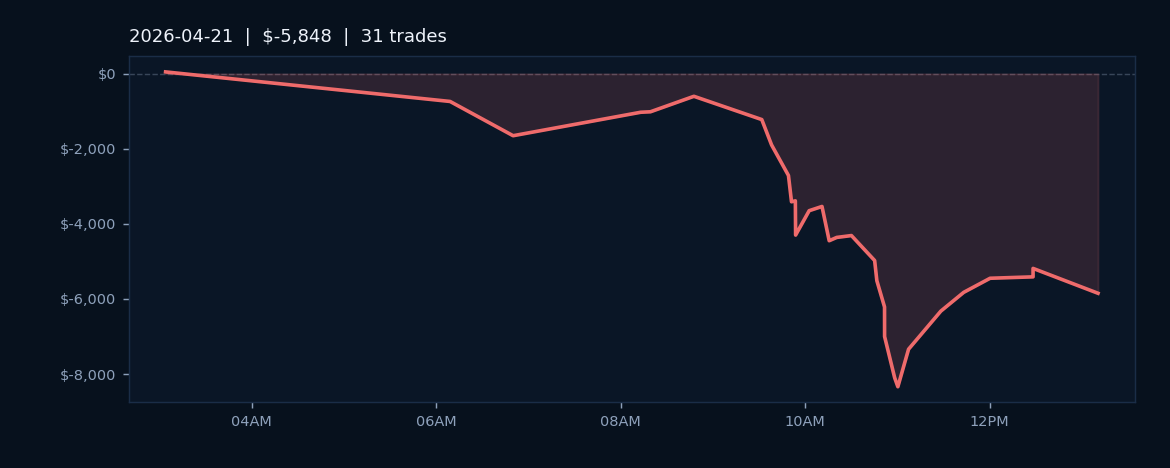

On Tuesday, April 21, 2026, GoodInvestGroup AlgoLabs OS executed 31 trades across three core indices: ES, MES, and NQ. The session closed with a net loss of $5,847.50, marking a challenging day despite maintaining a respectable win rate of 51.6%. The spread between winning and losing trades reflected typical intraday volatility, with the slight edge in win percentage insufficient to overcome the realized drawdown across the session's total volume.

The 51.6% win rate demonstrated that directional conviction was present in more than half of executed positions, yet the magnitude of losses outweighed gains when aggregated. This pattern is consistent with days when market microstructure or volatility regimes shift unexpectedly, compressing favorable risk-to-reward ratios. Trading across ES, MES, and NQ meant exposure across large-cap equities and tech-heavy indices, both of which experienced notable intraday range compression relative to session opening levels.

The $5,847.50 loss represented a session-level drawdown that traders and portfolio managers would monitor as part of standard monthly performance tracking. While individual days with negative P&L occur regularly in algorithmic trading, the relatively high trade count (31 executions) suggested the algorithms remained active and responsive to perceived opportunity rather than sitting idle. The data from April 21st underscored the importance of position sizing and stop-loss discipline, with implications for how subsequent trading sessions would calibrate risk parameters.