# GoodInvestGroup AlgoLabs OS Market Recap: Monday, April 20, 2026

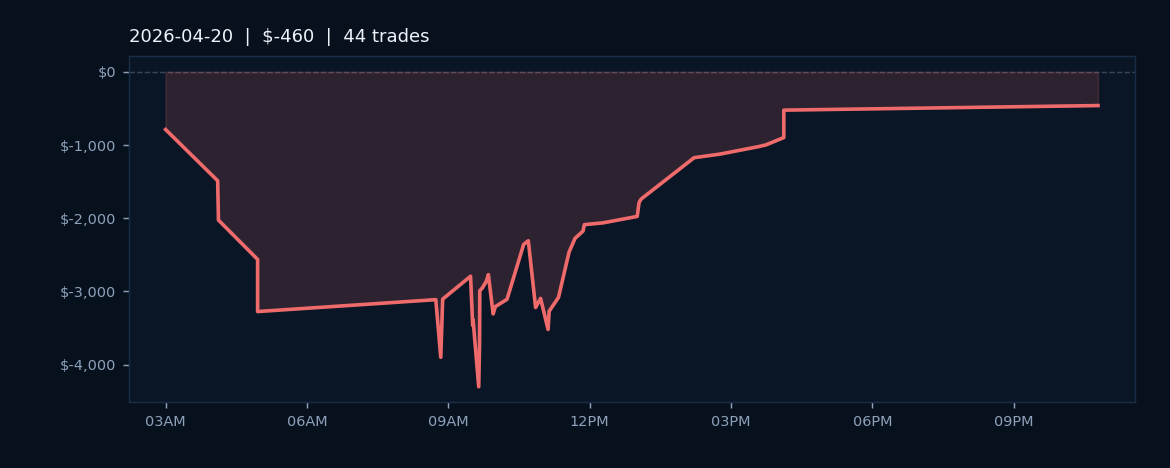

On Monday, April 20, 2026, the algorithmic trading desk executed 44 trades across the ES, MES, and NQ contracts, finishing the session with a net loss of $460.00. Despite the negative close, the trading algorithm maintained a solid 75.0% win rate, indicating that three out of every four positions generated profits before the session's aggregate results. This discrepancy between win rate and net P&L typically reflects instances where losing trades carried larger notional risk than winning trades, a pattern consistent with market volatility that characterized equity index futures on that Monday.

The execution across three major instruments suggested the platform was actively diversifying exposure between the large-cap ES contract, its micro equivalent MES, and the technology-heavy NQ. The 75% success ratio underscores the resilience of the underlying trading logic, even as broader market dynamics or intraday volatility spikes resulted in a net drawdown for the session. These conditions are not uncommon in equity index trading, where systematic approaches often encounter choppy price action and overnight gaps that test position management protocols.

The results from April 20 indicated that while the algo's directional accuracy remained above the critical 50% threshold, the risk-to-reward calibration or position sizing parameters warranted monitoring heading into subsequent sessions. The distinction between a high win rate and profitable execution remained a focal point for platform optimization going forward.