# GoodInvestGroup AlgoLabs OS: Week in Review

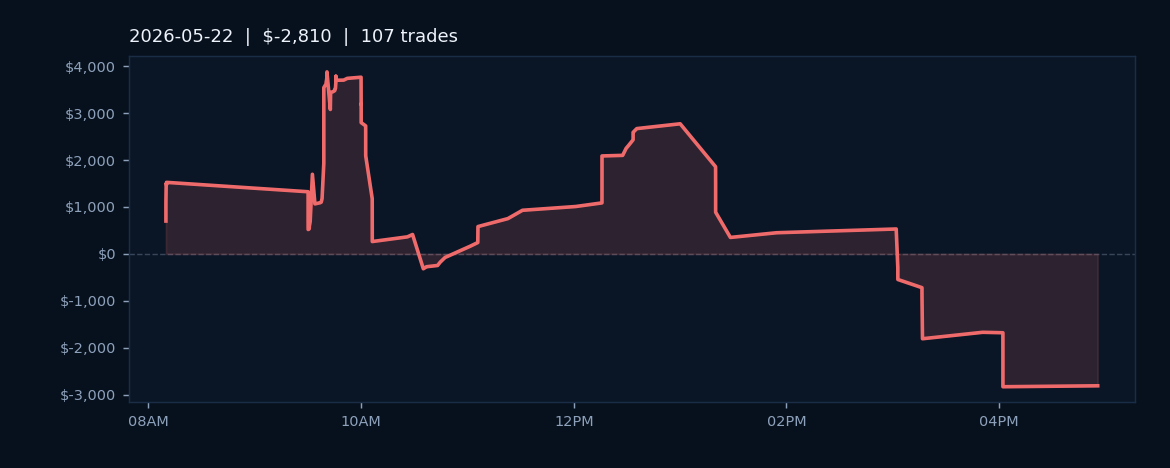

Friday, May 22, 2026 closed with mixed results across our crude oil and equity index strategies. The platform executed 107 trades throughout the session, maintaining a respectable 63.6% win rate across CL, ES, MES, MNQ, and NQ contracts. Despite the favorable hit rate, the session closed with a net loss of $2,809.74, reflecting a pattern where winning trades held insufficient edge relative to losses when they occurred. This outcome underscores the reality that win rate alone does not determine profitability; position sizing and risk management at the point of exit proved decisive in Friday's trading environment.

The distribution across five instruments indicated balanced exposure, though the consolidation in crude oil prices and lateral movement in both the ES and NQ futures created choppy conditions. Traders utilizing the platform experienced the challenges typical of low-volatility, range-bound sessions where technical reversals often triggered false breakouts. The 63.6% win rate demonstrated the platform's pattern recognition remained operational, yet the cumulative losses on unsuccessful trades exceeded cumulative gains, a dynamic common when market structure shifts to favor mean reversion over directional conviction.

Friday's performance served as a calibration moment rather than a setback. The session's data reinforced the importance of dynamic position management during periods when intraday volatility contracted relative to the prior week's range. The net result for May 22 suggested that the following trading week would benefit from closer attention to market microstructure and volatility regimes when determining appropriate entry and exit parameters.