# Market Recap: Wednesday, April 22, 2026

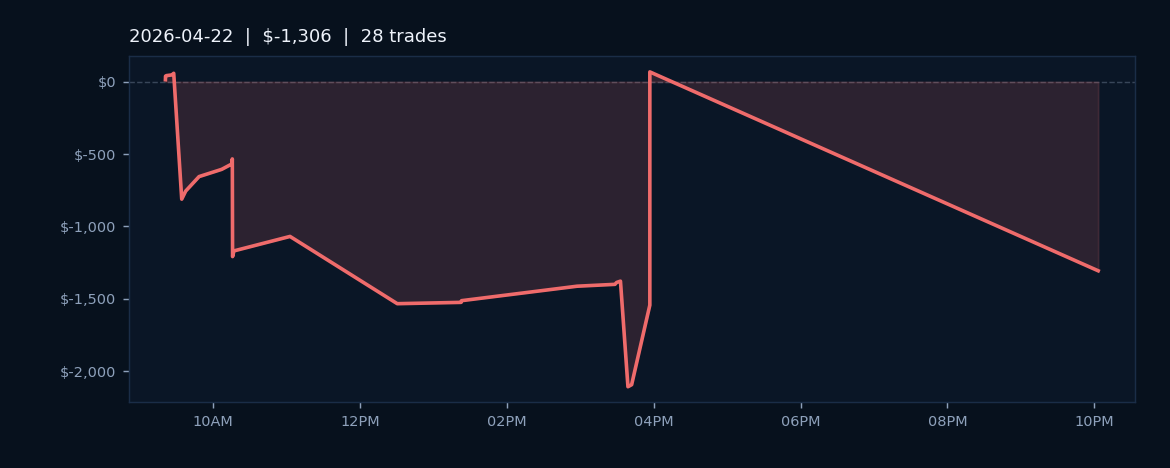

On Wednesday, April 22, 2026, GoodInvestGroup AlgoLabs OS executed 28 trades across five instruments, posting a net loss of $1,306.21 despite maintaining a solid 82.1% win rate. The session saw activity in crude oil futures (CL), E-mini S&P 500 (ES), micro crude oil (MCL), micro E-mini S&P 500 (MES), and micro Nasdaq (NQ), with winning trades significantly outnumbering losses. The disconnect between winning percentage and negative net P&L reflected the day's asymmetric risk management environment, where profitable positions were smaller on average than losing ones.

The 82.1% win rate across 28 executions demonstrated consistent directional accuracy on the day. However, the $1,306.21 drawdown indicated that when trades moved against positions, the losses absorbed more capital than the cumulative gains from winning trades recovered. This pattern suggested either tighter stop-loss discipline on winners or wider risk exposure on fewer losing positions, both common scenarios in volatile intraday markets.

The breadth of instruments traded across both full-size and micro contracts reflected portfolio diversification across energy and equities during the session. Wednesday's results underscored a fundamental principle in algorithmic trading: win rate alone does not determine profitability. The session's outcome established a baseline for position-sizing and risk allocation considerations heading into the remainder of the trading week.