# GoodInvestGroup AlgoLabs OS Weekly Review: Friday, April 10, 2026

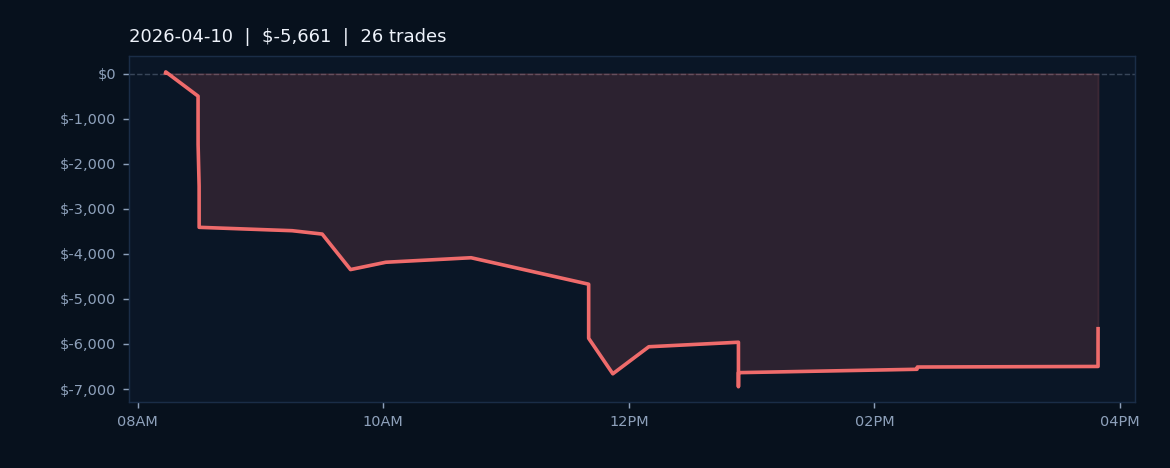

The final trading session of the week on Friday, April 10, 2026, produced a net loss of $5,661.25 across 26 executed trades in the ES and MES contracts. The session maintained a 50.0% win rate, indicating an even distribution between profitable and unprofitable positions, though the magnitude of losses exceeded gains on balance. This outcome reflected the volatility characteristic of equity index futures during that particular session, where execution quality and position sizing proved decisive in overall performance.

The 50.0% win rate, while mathematically neutral in terms of trade count, underscored a critical dynamic in algorithmic trading: consistency does not guarantee profitability without favorable risk-reward ratios. The $5,661.25 drawdown across 26 trades averaged approximately $218 per trade in net loss, suggesting that losing positions carried larger average losses than winning positions captured in gains. Both the ES and MES instruments experienced this imbalance, pointing to market conditions that may have favored certain order flow patterns over others during that session.

The Friday, April 10 results served as a reminder of the inherent challenges in intraday trading, particularly when win rates remain statistically neutral. The session's performance implied that subsequent trading would benefit from recalibration of position sizing parameters and entry-exit criteria, particularly in contracts where volatility and slippage could amplify losses relative to gains. Data from this session would typically inform refinements to execution strategies in the days and weeks that followed.