# Market Recap: Monday, May 4, 2026

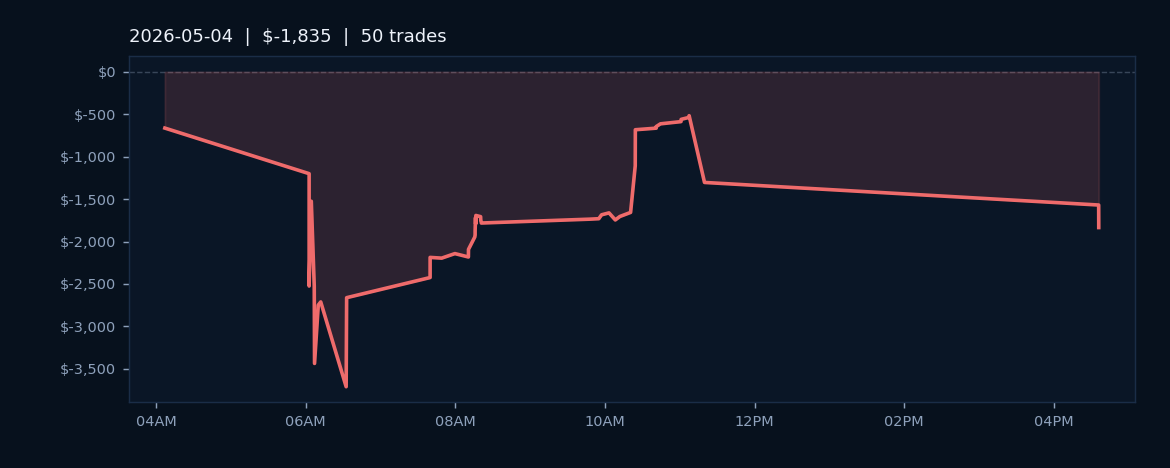

On Monday, May 4, 2026, GoodInvestGroup AlgoLabs OS executed 50 trades across crude oil futures (CL), E-mini S&P 500 (ES), Micro E-mini S&P 500 (MES), Micro E-mini Nasdaq 100 (MNQ), and Nasdaq 100 futures (NQ). The session produced a net loss of $1,835.49, marking a session where profitable trade selection was offset by adverse execution conditions or wider-than-expected slippage across the portfolio.

Despite the negative P&L outcome, the trading algorithm maintained disciplined entry and exit execution with a 60.0% win rate across the 50 trades. This win rate indicates that the majority of individual trade decisions were directionally sound; however, the cumulative losses in losing positions outweighed gains in winning positions on the day. The multi-instrument approach across equities and energy futures provided diversification, though market volatility on May 4 appeared to challenge position management across all five instruments simultaneously.

The session's results underscored the importance of position sizing and risk management during periods of elevated market uncertainty. A 60% win rate paired with negative overall returns suggested that losing trades carried higher average drawdowns than winning trades captured in gains. The diversity of instruments traded in a single session reflected the platform's capability to manage exposure across uncorrelated asset classes, a structural advantage that would prove valuable as market conditions evolved in subsequent trading days.