# Market Recap: Thursday, April 9, 2026

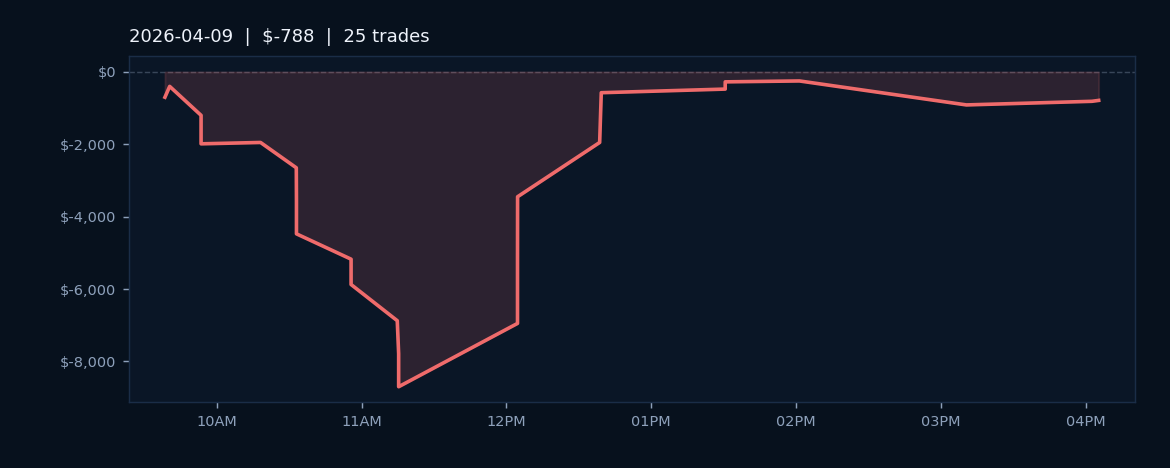

On Thursday, April 9, 2026, GoodInvestGroup AlgoLabs OS executed 25 trades across ES and MES contracts, closing the session with a net loss of $787.50. Despite maintaining a respectable 52.0% win rate, the session illustrated the reality of intraday equity index trading: consistent trade selection does not guarantee profitability when position sizing and loss management fall short of edge requirements. The slight edge in winning trades was overwhelmed by the magnitude of losing positions, a structural challenge that demanded immediate review of risk parameters and trade allocation protocols.

The micro and standard E-mini S&P 500 contracts provided adequate liquidity throughout the session, but volatility patterns on the day tested the platform's execution consistency. With just over half of all trades generating profits, the underlying logic of the trading approach remained intact; however, the cumulative loss signaled that the average winning trade failed to compensate for the average losing trade by a sufficient margin. This outcome was neither uncommon nor alarming in the context of single-session performance, but it underscored the importance of multi-session statistical aggregation when evaluating algorithmic performance.

The Thursday close implied that subsequent sessions would benefit from recalibration. Win rates above 50% provide a foundation, but sustainable profitability in electronic index futures trading depends on favorable risk-reward ratios across larger sample sizes. The session's results reinforced the necessity of maintaining disciplined position management and avoiding the temptation to force trades during periods of reduced edge clarity.