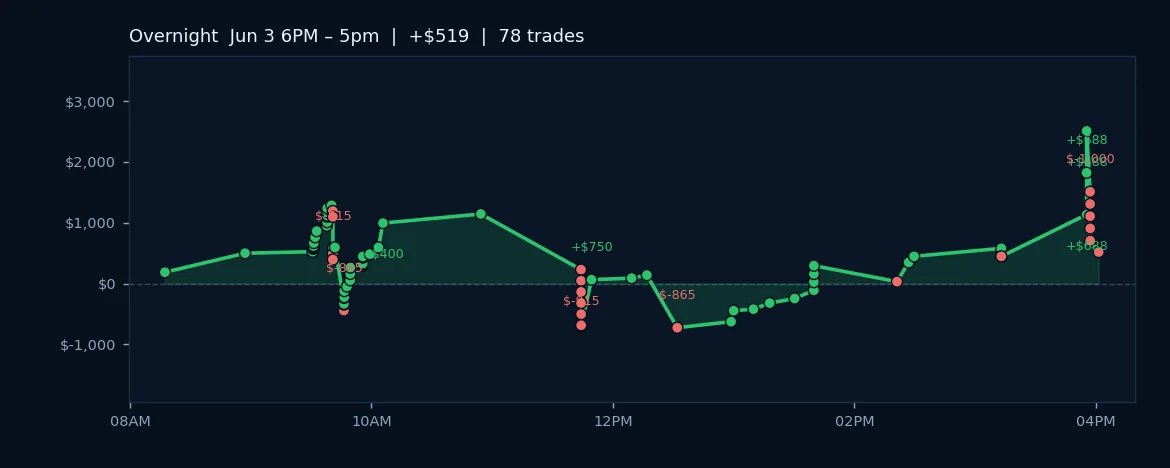

The desk closed Thursday with 78 trades executed and a net gain of $518.84, though the 71.8% win rate masks a critical operational insight: specific hourly windows are systematically eroding returns. AI Sentiment remains negative with confidence holding at 62.0% (AI Pi), and the regime filter continues to register trend mode at maximum conviction. The session reinforced what our backtests have been signaling for weeks: not all hours are created equal, and rigid time-of-day filters could materially improve risk-adjusted performance going forward.

The most actionable signals emerging from today's analysis point to two distinct problem zones. The midday window spanning 12:00 to 13:00 ET has generated a cumulative -$1,265 loss across historical trades, averaging -$74.41 per trade during those two hours alone. Separately, pre-market trading from 06:00 to 07:59 ET has proven even more destructive, with the 06:00 and 07:00 ET buckets combining for -$3,712.50 in losses. These aren't noise; they're statistically significant drains that demand algorithmic discipline.

Complementary pattern recognition has identified structural calendar effects worth monitoring. Monday trading has yielded -$4,000.00 net across 35 trades, making it the weakest day of the week, while Tuesday adds measurable drag as well. Against this backdrop, the algos are recommending a daily loss limit of $1,598 as a data-grounded guardrail, calibrated to the observed distribution of losing days. Tomorrow's employment data (Average Hourly Earnings, Non-Farm Employment Change, and Unemployment Rate) will test market structure once more, but the desk is now watching whether tighter time-of-day gating and day-of-week filters can unlock the gains hidden in today's win rate.