For more than a decade, retail brokerage operated on a simple and seductive promise.

Zero commissions. Free trading. Democratized markets.

It worked. Retail participation exploded. Millions of new accounts opened. A generation of traders who might have been priced out of active market participation found themselves with direct access to equities, options, and ETFs — all for the apparent cost of nothing.

Except trading was never free. The cost was simply hidden.

And now, as regulatory pressure mounts on both sides of the Atlantic and the SEC moves toward a fundamental restructuring of order routing, the most important subsidy in retail finance is facing its long-delayed reckoning.

The Mechanism Nobody Explained at Account Opening

Payment for order flow is a legal arrangement in which brokerages sell the right to execute customer trades to third-party market makers.

When you click buy on 100 shares of a large-cap stock, your order does not necessarily go to the New York Stock Exchange. It goes, in most cases, to a market maker — Citadel Securities, Virtu Financial, or similar — who pays your broker a fraction of a cent per share for the privilege of executing your trade.

The market maker's profit comes from the spread. They buy from you at the bid and sell at the ask, or vice versa, capturing the difference. They pay the broker a portion. You receive what appears to be a competitive fill price — and your broker reports zero commission charged.

The system worked because for many trades — particularly large-cap stocks in liquid markets — the price improvement was real. You might have paid a penny less per share than the quoted bid-ask spread. Market makers competed to provide better fills. Everyone benefited.

Or so the story went.

The Fill Quality Problem

The academic and regulatory literature on PFOF tells a more complicated story.

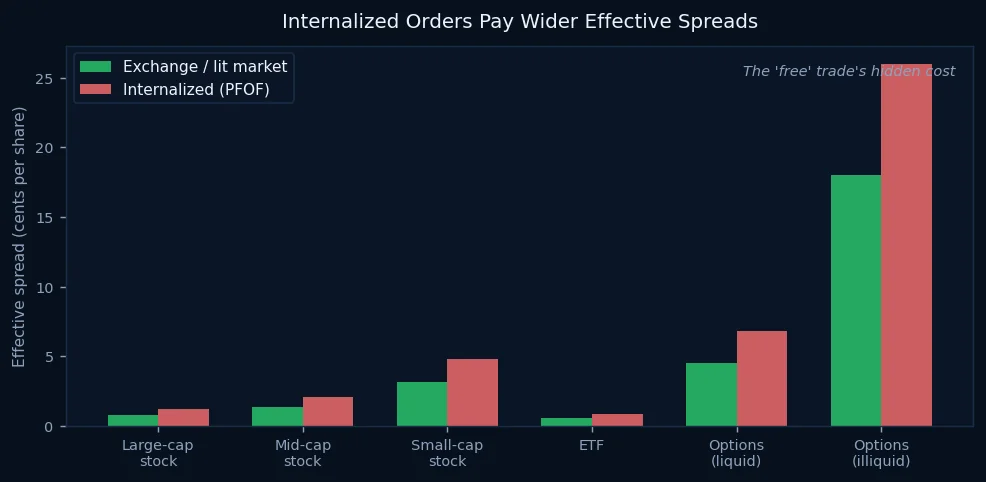

When retail orders are internalized — executed off-exchange by a market maker — they are systematically excluded from the price-setting process. They do not contribute to price discovery. They do not narrow spreads on public exchanges. And they often receive fills that are technically better than the quoted spread, but significantly worse than what a midpoint execution on a lit exchange would have delivered.

The gap is smallest in the most liquid securities — the Apples and Teslas of the world where competition is fierce and spreads are already razor-thin. It grows substantially in mid-cap stocks, small-caps, and options — exactly the assets where active retail traders tend to focus.

For a trader executing dozens of trades per week, the aggregate cost of suboptimal fills is not theoretical. It compounds. It drags on performance. And it was never disclosed.

Where Your Order Actually Goes

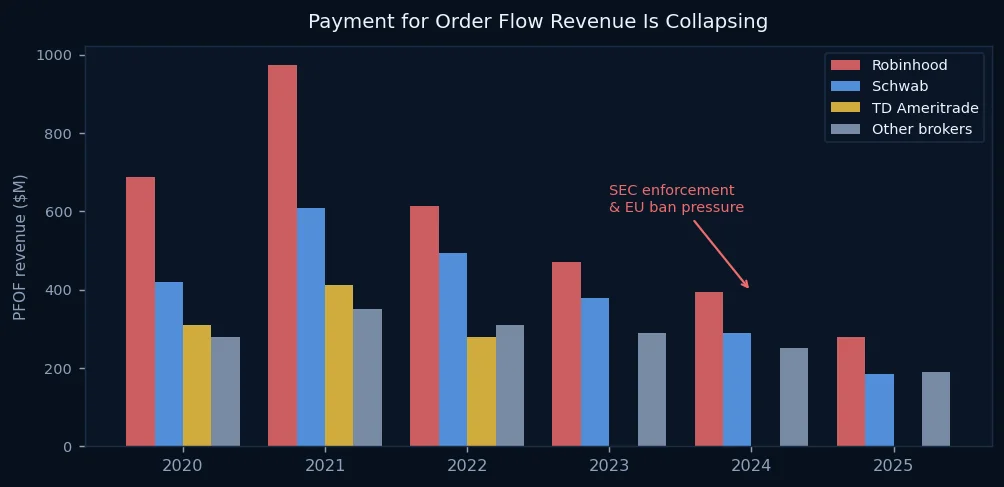

The EU banned payment for order flow entirely in 2026 for most instruments. The UK followed. The SEC's revised best execution rules — long delayed, repeatedly contested — are now forcing US brokers to demonstrate, in granular detail, that their routing choices actually serve client interests.

The result: PFOF revenue at major US brokers has declined significantly from its 2021 peak. Robinhood, whose entire business model was built around PFOF, has been forced to diversify into margin lending, crypto, and subscription products. Schwab and others are navigating the same transition.

What Comes After Free

The post-PFOF era will not look like the pre-PFOF era. The genie of zero commissions is out of the bottle — brokers cannot simply return to charging $9.99 per trade.

Instead, the industry is moving toward a hybrid model: subscription tiers, premium order routing options, and explicit best-execution guarantees that allow sophisticated traders to pay for demonstrably better fills.

For active traders — particularly those running systematic or algorithmic strategies where fill quality directly affects performance — this may actually be an improvement. Paying $1 per trade for midpoint execution on a lit exchange beats paying $0 for internalized fills that cost you $3 in slippage.

The free lunch is ending. But the meal that replaces it may be more honestly priced.

And in markets, honest pricing is almost always a better starting point than a hidden subsidy.