For more than two decades, the Pattern Day Trader rule stood as one of the most debated gates in American markets.

Four day trades within five business days? You were officially labeled a pattern day trader. And unless you maintained at least $25,000 in your brokerage account, the door largely closed.

To supporters, the rule was protection. To critics, it felt like financial classism wrapped in regulatory language.

Now, that era is ending.

Following regulatory approval, the traditional PDT framework is being phased out and replaced with a modern, risk-based intraday margin system. The infamous trade-counting mechanism that frustrated generations of active traders is finally heading toward retirement.

And the timing could not be more fascinating — because this shift is not happening in isolation.

It is arriving at the same moment markets are beginning to anticipate what could become one of the most explosive IPO environments in years, potentially involving names like SpaceX, OpenAI, and Anthropic.

The question is no longer whether PDT is disappearing. The real question is what happens when millions of retail traders face fewer barriers to active trading — precisely when some of the world's most captivating companies may be approaching public markets.

What Is Actually Changing?

This is where headlines can become misleading.

Regulators are not creating unlimited leverage or eliminating risk controls. The change is more nuanced. The traditional trade-counting framework is being replaced with a risk-based intraday margin model — meaning brokerages will increasingly focus on the actual exposure inside an account rather than how many trades a customer places.

No more PDT designation. No more four-trades-in-five-days counting rule. No universal $25,000 threshold.

In its place: greater broker risk monitoring, real-time surveillance of account exposure, and margin management that adapts to behavior rather than counting it.

Some firms will move quickly. Others will adapt more gradually as compliance infrastructure catches up. The experience will vary significantly by broker. And while the old restriction is disappearing, broker risk engines are becoming increasingly sophisticated.

The result is not "anything goes." It may be more accurate to describe it as freedom with surveillance.

Retail Already Found Workarounds

PDT never completely stopped active trading. Retail traders adapted — they always do.

Cash accounts. Futures markets. Multiple brokerage accounts. Prop-firm structures. The limitation became less of an impenetrable wall and more of a source of friction.

Which raises an important question: if workarounds already existed, what does eliminating PDT truly change?

The answer may be surprisingly simple: psychology.

The old framework made active trading feel restricted. The new one may make it feel normal. And that distinction — purely psychological — may matter more than any regulatory detail.

The Bull Case: Modernization, Not Recklessness

Supporters argue the change is overdue.

The original PDT system was designed for a different era — early internet brokerages, slower technology, far less sophisticated monitoring. Markets today look very different. Broker systems track risk continuously. Margin engines operate dynamically. Surveillance tools are more advanced than regulators could have imagined in 2001.

Why preserve a rigid trade counter when risk itself can already be measured more precisely? A trader with $24,999 and disciplined risk management posed no more danger than one with $25,001 in account equity. The barrier was always more connected to account size than to actual behavior.

The Bear Case: A New Trading Acceleration Cycle

But every reduction in friction carries a second side.

Markets do not operate on mathematics alone. They operate on emotion. And emotion moves fast.

Lower barriers encourage greater participation — but they may also encourage greater speculation. We have seen versions of this story before: meme stocks, zero-commission explosions, options trading surges, financial influencers turning markets into entertainment.

The concern is not merely that more people will trade. It is that trading may become increasingly gamified.

The Timing Question

The broader backdrop makes this moment particularly interesting.

SpaceX remains one of the most anticipated potential IPO candidates in history. OpenAI continues reshaping technology and capital markets. Anthropic has emerged as one of the most closely watched companies in artificial intelligence.

None of this guarantees immediate listings. But anticipation alone carries power — IPO cycles are emotional events as much as financial ones. They create stories, excitement, and retail participation.

Easier access combined with powerful narratives can generate extraordinary market energy — sometimes productive, sometimes destabilizing, often both.

The Advantage Algorithmic Traders Already Had

One group never particularly cared about PDT: algorithmic and futures traders.

Futures markets — ES, NQ, MNQ, CL — have always operated entirely outside PDT restrictions. There is no four-trade limit, no $25,000 threshold, no counting mechanism. Active algo strategies can execute dozens of trades per session without regulatory friction. Risk is managed at the position and margin level, not through trade-count surveillance.

In that sense, the new retail framework is simply catching up to what systematic traders have always known: trade frequency is the wrong metric. Exposure and risk management are what matter.

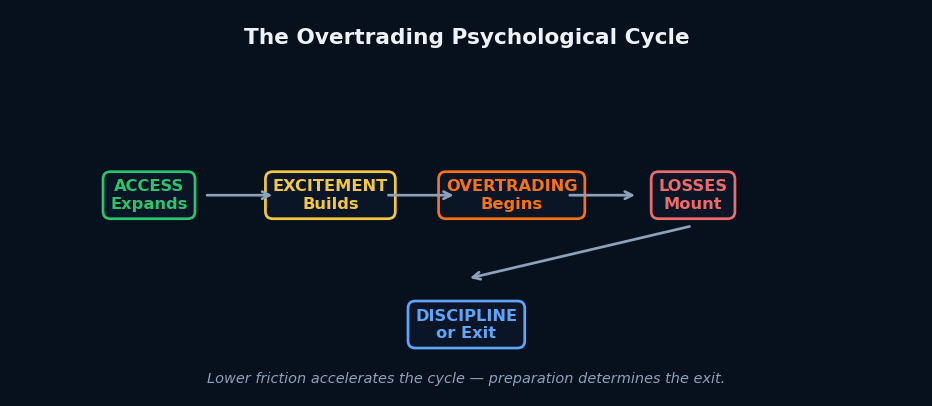

The Part No Rule Can Solve

The removal of PDT may change market access. It does not change human nature.

While regulators can redesign margin frameworks, they cannot regulate impulse, fear, greed, or overconfidence. For many traders, the greatest challenge was never the four-trade limit — it was what happened after the limit disappeared.

Overtrading remains one of the most common psychological traps in active markets. More trades do not create better results. Experienced traders often discover the opposite: fatigue builds, emotions compound, revenge trading appears, and decision-making deteriorates when activity becomes constant.

Markets rarely punish lack of intelligence alone. More often, they punish lack of discipline.

Perhaps that is the hidden irony beneath the entire PDT debate. The hardest limit in trading was never the regulatory one. It was always the psychological one.

The Real Takeaway

The death of PDT will trigger celebration across retail trading communities — and many of those celebrations will be understandable. The old rule frustrated traders for years.

But declaring this a complete victory may be premature. While the trade counter is disappearing, risk itself is not. The new era may offer greater opportunity. It will almost certainly demand greater discipline.

Regulators did not abolish danger. They simply changed how responsibility is measured.

The coming years will reveal whether this transition creates healthier markets or merely faster speculation. But one thing already appears clear: the era of the trade counter is ending, retail trading is evolving, and markets may be entering one of their most fascinating chapters in decades.