On June 12, 2026, SpaceX began trading on the Nasdaq under the ticker SPCX.

The numbers are staggering. Seventy-five billion dollars raised. One point seven five trillion dollars in implied valuation. More money changing hands in a single IPO than the entire GDP of many developed nations.

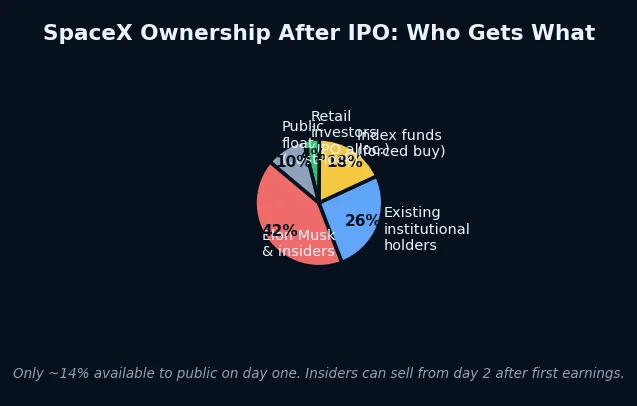

And at least thirty percent of those shares allocated, Elon Musk has suggested, to retail investors.

This is being celebrated in many quarters as democratization. The biggest private company in American history finally accessible to everyday investors. A chance to participate in the space economy at the ground floor.

A more careful reading of the mechanics suggests something different.

The Largest Transfer in IPO History

Context first.

SpaceX raised more in its IPO than Alibaba, Saudi Aramco, and every other IPO in recorded history — combined. The $75 billion figure represents not just the scale of the offering but the ambition of the exit strategy: insiders converting private valuation into public liquidity at a price set by institutional demand and amplified by index inclusion mechanics.

The valuation of $1.75 trillion is real only in the sense that it reflects what someone was willing to pay on June 12. Whether that price reflects the present value of future cash flows from Starship, Starlink, and government contracts — or reflects the momentum of narrative and forced index buying — is a question the market has not yet been forced to answer.

The Float Problem Nobody Is Talking About

SpaceX went public with approximately 5% of shares in the public float.

This is a structural feature, not an oversight. Low float IPOs create scarcity — which drives price, which generates headlines, which attracts retail buying. The mechanics are self-reinforcing on the way up.

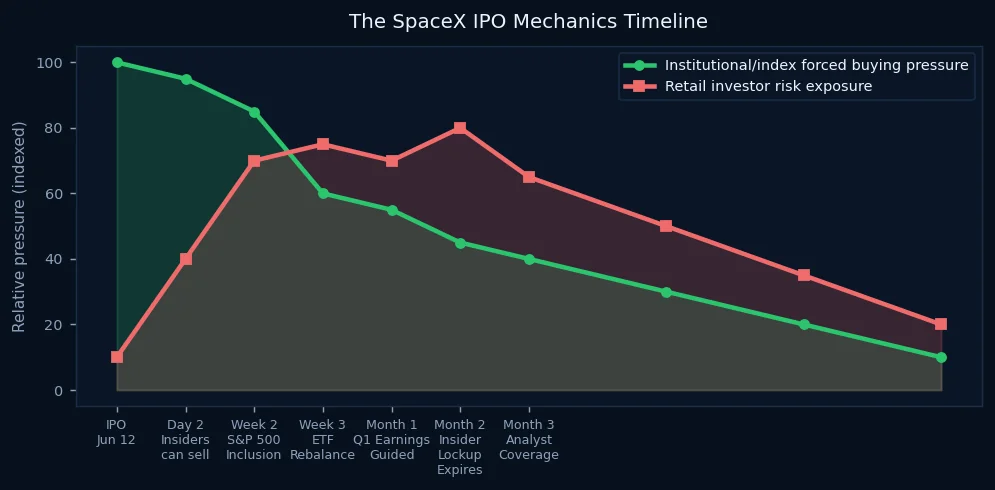

The more consequential structural feature is index inclusion. Index providers waived the standard profitability requirement for SpaceX and cut the seasoning window from 90 days to 5 — meaning the S&P 500 and Nasdaq-100 were required to include SPCX within the first week of trading.

Over $30 trillion in passive 401k and retirement capital tracks these indices. When a stock is added, every index fund must buy it in proportion to its weight. That buying is not discretionary. It is mechanical. It happens regardless of valuation.

In the case of SpaceX, that forced buying represents roughly $180-220 billion in required purchases from passive vehicles alone — at whatever price the market has set after the IPO. The buyers have no price sensitivity. They must own the stock.

The Insider Timeline

The design of SpaceX's lockup provisions deserves particular attention.

Standard IPO lockups prevent insiders from selling for 180 days. SpaceX established a staggered structure in which insiders can begin selling as soon as the second trading day after the first quarterly earnings release — expected in August 2026.

This means: retail investors who buy at IPO prices in June are buying stock that insiders can begin systematically selling in approximately 60-70 days. The gap between when retail capital enters and when insider supply arrives is narrow.

This is not illegal. It is the designed mechanics of how IPOs work. But retail investors who do not understand this timeline may find themselves on the wrong side of a supply imbalance they did not anticipate.

What This Means for Algo Traders

The SpaceX IPO creates several distinct dynamics that systematic traders should track.

Sector rotation pressure: A $75 billion raise pulls capital from somewhere. Institutional investors who participated in the SpaceX book are underweight in other positions. Expect sector rotation signals in the weeks following the IPO.

Volatility expansion: Low-float, high-narrative stocks trade with extreme volatility. SPCX will likely trade in wide daily ranges as the market discovers its true equilibrium. For momentum systems tuned to established equities, the SpaceX volatility signature will be a statistical outlier.

Index rebalancing flows: The forced buying from passive vehicles is mechanical and time-constrained. When it ends, the artificial price support ends with it.

SpaceX may be an extraordinary company. Starship is genuinely transformative technology. Starlink has already demonstrated commercial scale. The business case is real.

But business case and IPO price are two different things. And the mechanics of a $75 billion, 5% float offering with staggered insider selling and forced index inclusion are not designed primarily to benefit the retail investor who clicks Buy on June 12.

The floor is uncertain. The ceiling is imagination. And between them sits the mechanism.