Something quiet happened in early 2026 that most equity-focused traders missed entirely.

The meme trade moved.

Not to a new stock. Not to crypto. Not to some obscure small-cap. It moved to crude oil and silver — physical commodities with real delivery obligations, finite supply chains, and no circuit breakers.

This is not a small development. It may be one of the most structurally important shifts in retail market behavior since the GameStop era.

And almost nobody is writing about the mechanics of why it changes everything.

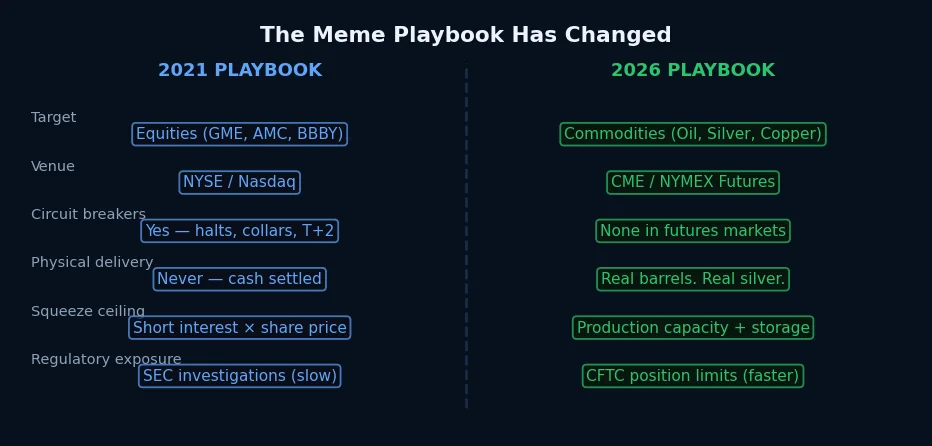

The Playbook Is the Same. The Arena Is Not.

The retail coordination playbook has not changed. Social platforms still host the discussions. Options are still the preferred leverage vehicle. The psychology is identical — identify a heavily shorted or constrained asset, concentrate buying pressure, force a mechanical squeeze.

But the venue has shifted.

In 2021, the target was equities — stocks listed on exchanges with circuit breakers, trading halts, T+2 settlement, and SEC oversight with subpoena power. Short sellers in equities can wait. Borrow shares, pay the fee, ride out the volatility. The worst outcome is an expensive position, not a logistics problem.

Commodities are different.

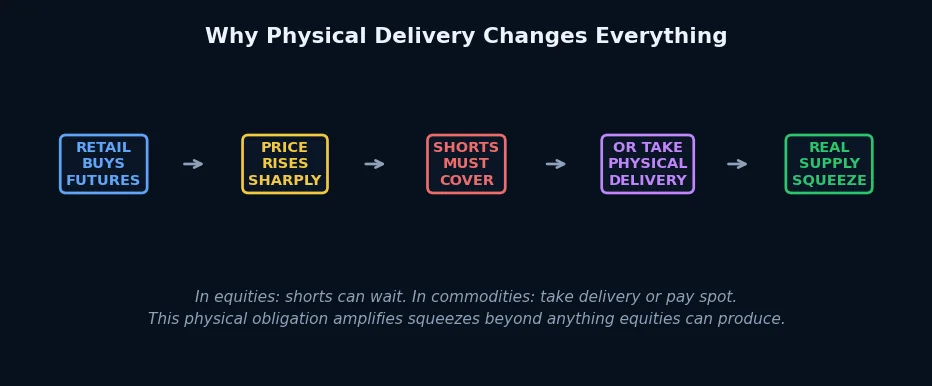

When retail money floods into crude oil futures or silver contracts on the CME, the shorts face a choice that equity shorts never face: cover at market price, or take physical delivery.

Not theoretical delivery. Not cash settlement. Actual barrels of oil. Actual silver bars.

That distinction is not a footnote. It is the entire mechanism.

What Happened in April 2026

Following US military strikes near Venezuelan oil infrastructure and renewed escalation in the Middle East, retail traders — already primed from years of zero-commission options access — pivoted aggressively into energy and precious metals.

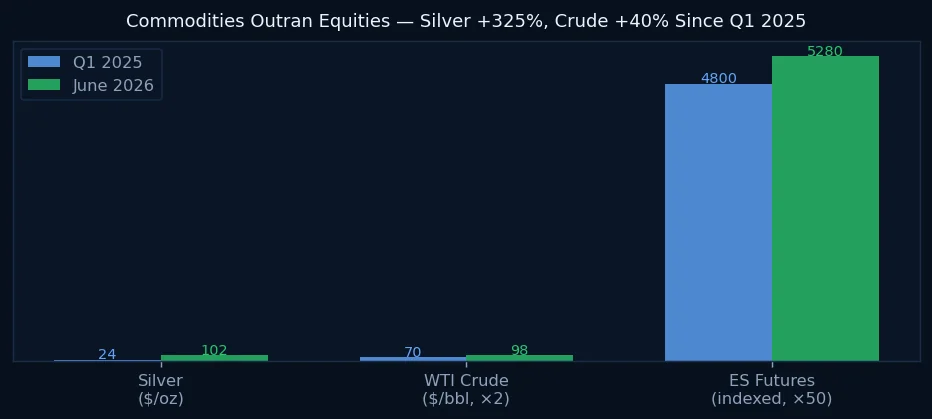

Silver broke $100 per ounce for the first time in recorded history.

Crude oil front-month futures experienced intraday swings exceeding fifteen percent on three separate days in March and April — moves that in equities would have triggered market-wide halts.

In the futures markets, there were no halts.

Position limits exist in theory. The CFTC monitors concentration. But the coordination was diffuse — thousands of smaller accounts, each below the threshold that triggers regulatory review, collectively moving contracts that carry real-world supply implications.

This is not hypothetical. During the April crude spike, storage operators in Cushing, Oklahoma — the delivery point for WTI futures — reported unusual inquiry volume from financial counterparties attempting to understand physical acceptance procedures.

That detail matters. It means retail-driven futures positioning was close enough to the delivery mechanism to create genuine operational concern.

Why Commodities Amplify Beyond What Equities Can

The meme stock era produced extraordinary short squeezes. GameStop rose from $5 to $483 in under a month. But every dollar of that move was purely financial — shares exchanged, losses absorbed, eventually unwound.

Commodity squeezes have a physical ceiling that equities do not.

When a futures contract approaches expiry, open interest must resolve. Every short position must either be covered in the market — at whatever the market price is — or accepted as physical delivery. Producers cannot instantly expand output. Refiners cannot instantly increase capacity. Warehouses have finite space.

This creates what physicists might call a hard constraint on the short side.

An equity short seller facing a squeeze can, in theory, hold indefinitely and absorb pain. A commodity short facing physical delivery has a hard deadline: the first notice day of the contract. After that, the option to wait evaporates.

This is why commodity squeezes, when they occur, tend to be faster and more violent than equity squeezes. The 2021 natural gas crisis in Europe demonstrated this at a sovereign level. The Hunt Brothers silver squeeze of 1980 demonstrated it at the market level.

The 2026 version is being driven by retail, operating through fractional futures contracts and micro-lot sizing that did not exist in 1980. The coordination infrastructure has improved. The underlying physical constraint has not changed.

The Circuit Breaker Problem

Equity markets have multiple layers of protection against runaway price action. Individual stock halts. Market-wide circuit breakers at seven, thirteen, and twenty percent drops. Regulatory authority to halt trading in specific securities under extraordinary circumstances.

Futures markets have limit up and limit down rules — but these operate differently. A contract hitting its daily limit does not halt; it simply cannot trade beyond that price. This can create cascading pressure when the market reopens the following session.

More importantly: limits do not prevent the delivery obligation. A crude contract that hits limit-up ten days in a row still requires resolution at expiry.

The CFTC has position limit rules, but enforcement is slower and less predictive than the SEC's circuit breaker infrastructure. By the time a formal investigation opens, the squeeze has typically resolved — one way or another.

What This Means for Algo Traders

For algorithmic strategies operating in equity futures — ES, NQ, MNQ — the implications are indirect but real.

Commodity volatility transmits to equity markets through multiple channels. Energy cost shocks affect corporate earnings expectations. Silver and copper prices are leading indicators of industrial demand. Oil volatility creates positioning pressure in macro funds that simultaneously hold equity exposure.

When retail-driven commodity moves produce outsized intraday swings, correlation regimes shift temporarily — strategies calibrated on normal correlation assumptions can encounter regime breaks that look like model failure but are actually macro contamination.

The more immediate implication: volatility in energy commodities tends to precede equity volatility by days to weeks. If oil is experiencing coordinated retail squeezes, the signal for equity positioning should adjust accordingly.

The Bigger Picture

The meme trade moving into commodities is not a passing phase. It reflects a maturing retail market that has exhausted the easy equity targets — most heavily shorted small-caps are now defensively positioned against retail squeeze campaigns — and discovered an asset class where the supply constraints are real and the regulatory response is slower.

This does not mean commodity squeezes will succeed every time. Most will not. The Hunt Brothers ultimately lost. Natural gas shorts in 2021 eventually recovered their positions.

But the structural shift in where retail coordination energy is being directed represents a genuine change in market microstructure. Commodity markets were not designed to absorb coordinated retail demand the way equity markets have adapted to.

That gap is now being tested.

Whether it produces a genuine historical squeeze or simply elevated volatility and a CFTC rulemaking, the playbook has permanently expanded.

Equity-only traders who do not track commodity positioning are now operating with an incomplete map.