Artificial intelligence did not sneak into financial markets. It arrived loudly, with press releases and product launches and breathless coverage about the death of human trading.

What arrived quietly — without press releases, without coverage, without anyone fully recognizing the systemic implication — was something more subtle.

The models started reasoning the same way.

Not because they were designed by the same teams. Not because they were given identical instructions. But because they were trained on the same internet, the same financial filings, the same news corpus, the same price history. And because the same macro conditions, the same earnings data, and the same sentiment signals flow through them simultaneously.

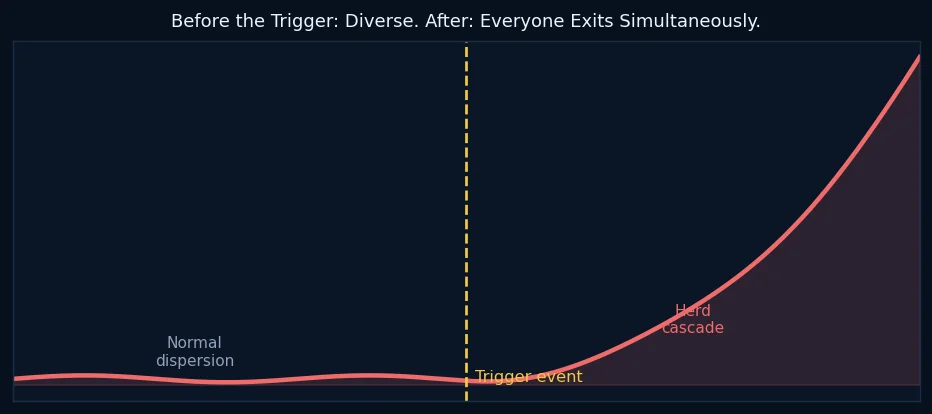

When independent systems make independent decisions from identical inputs, they are not independent.

They are a herd with unusually good communication skills.

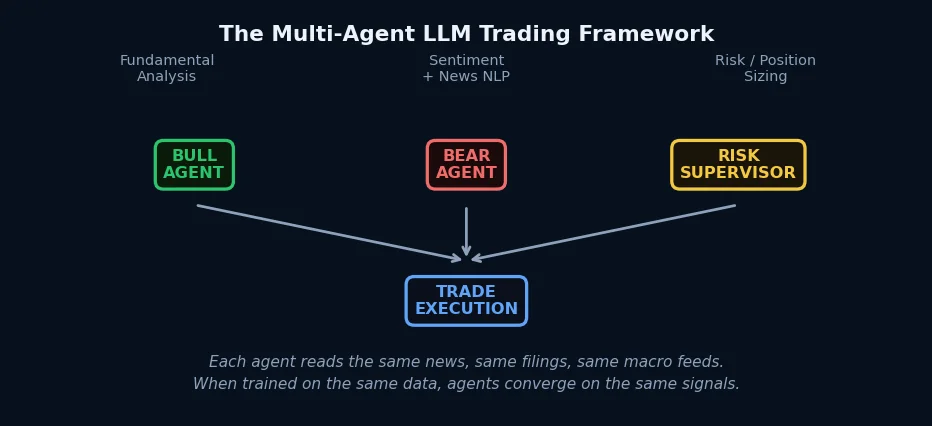

How Modern AI Trading Works

The dominant architecture for AI-driven trading in 2026 is the multi-agent LLM framework. Rather than a single model making all decisions, multiple specialized agents operate in parallel — one focused on fundamental analysis, one on sentiment and news interpretation, one on risk management and position sizing.

BlackRock's publicly described "Three-Layer" framework uses exactly this structure: a Bull agent, a Bear agent, and a Risk Supervisor that arbitrates between them.

This architecture is genuinely more sophisticated than earlier rule-based systems. The agents can incorporate qualitative information — earnings call transcripts, geopolitical news, Federal Reserve communications — in ways that traditional quantitative models cannot. They can explain their reasoning in natural language. They adapt dynamically as market conditions change.

And they produce results. Multiple academic and industry evaluations have demonstrated that multi-agent LLM frameworks outperform both single-model approaches and traditional factor-based strategies on a risk-adjusted basis.

The research is compelling. The deployment is accelerating. By current estimates, sixty to seventy percent of equity volume is now algorithm-driven, with LLM-based frameworks representing a growing share of that number.

Which creates the problem nobody wants to discuss.

The Identical Input Problem

Every major LLM used in financial applications — GPT-4 class models, Claude, Gemini, the frontier models deployed at institutional scale — was trained on overlapping datasets. They read the same books, the same news archives, the same financial literature.

More importantly, the real-time data feeds that inform their trading decisions are the same.

When Apple reports earnings, every LLM reads the same press release, the same 10-Q filing, the same analyst commentary. When the Federal Reserve releases its minutes, every model processes the same document through architectures that have learned, from identical training data, how to interpret central bank language.

The conclusions will not be perfectly identical. Different training runs, different fine-tuning, different prompt engineering create real variation in outputs. But the directionality of those conclusions — buy or sell, risk-on or risk-off, increase or decrease exposure — will cluster in the same direction with much greater frequency than if the models were truly independent.

This is not a theoretical concern. Traditional algorithmic herding — momentum strategies all exiting simultaneously, risk parity funds all deleveraging together — has been documented and studied for decades. The 2010 Flash Crash, the August 2015 volatility event, the March 2020 liquidity crisis all had algorithmic coordination as a contributing factor.

LLM-based agents introduce a new dimension to this problem: they herd on qualitative narrative, not just quantitative signals.

When a geopolitical event occurs, traditional algos respond to price action. LLM agents respond to the news itself — before the price moves. If they all read the same news and reach the same qualitative conclusion, their trades arrive simultaneously, creating price impact before human traders have even processed the headline.

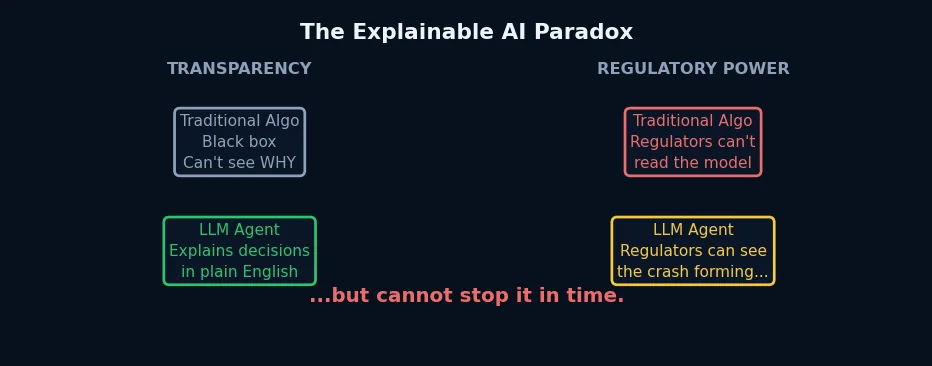

The Explainable AI Paradox

Here is where the story becomes genuinely strange.

For decades, regulators complained about black-box algorithms. They could see the trades. They could see the outcomes. But they could not see the reasoning. The model was opaque, and opacity made intervention nearly impossible.

LLM agents solved that problem. They are, by design, explainable. They produce natural language rationales for every decision. A regulator can read, in plain English, exactly why a system sold ten thousand contracts of ES futures at 9:47 AM.

This is progress. Genuine, meaningful progress. The regulatory community can now audit AI trading decisions in ways that were impossible with earlier systems.

But explainability does not equal interruptibility.

When a hundred LLM-based systems all read the same geopolitical news at 9:45 AM and all produce natural-language explanations for why they should reduce equity exposure simultaneously, the regulator can read every one of those explanations. They are transparent, coherent, and individually reasonable.

And the trades still execute simultaneously. The cascade still begins. The price impact still accelerates.

Explainability without the ability to intervene before execution is, in practice, a post-mortem capability. It tells you clearly what happened and why. It does not prevent it from happening.

This is the paradox: the most transparent AI systems in financial history may produce the most visible flash crash in financial history — and transparency will do nothing to stop it.

What Regulators Are Trying

The regulatory response is real but behind the curve.

New exchange rules now require unique strategy identifiers for algorithmic trading systems, enabling better post-trade attribution. Systems executing more than ten orders per second are classified as high-frequency and subject to additional scrutiny. FINRA has proposed mandatory stress testing for AI-driven strategies under coordinated market stress scenarios.

These are reasonable measures. They represent genuine regulatory learning from the failures of the 2010-2020 period.

But they operate on reporting timelines and supervisory frameworks designed for human decision speeds. An LLM-driven cascade can move faster than any current intervention mechanism can respond. By the time a circuit breaker activates, the price impact has already occurred.

The gap between the speed of AI decision-making and the speed of regulatory intervention is not closing. It is widening.

The Question Worth Asking

None of this argues that AI in trading is bad. The efficiency gains are real. The analytical capabilities are genuine improvements over what came before. Markets with sophisticated AI participation are, in many measurable ways, more liquid and better-priced than markets without it.

The question is not whether AI belongs in markets. It clearly does.

The question is whether markets have correctly priced the tail risk of coordinated AI behavior — the low-probability but high-consequence event where systems trained on identical data reach identical conclusions at identical moments.

Traditional flash crashes recovered. Liquidity returned. The market re-opened the next day.

A flash crash driven by coordinated LLM agents — occurring simultaneously across equities, fixed income, and currency markets, because all the agents read the same macro news — would be qualitatively different. Not necessarily larger. But structurally more complex to resolve, because the cause would be distributed across hundreds of independent systems rather than concentrated in a single product or strategy.

The frameworks exist. The regulation is being built. The transparency is there.

What does not yet exist is a mechanism to stop it.

That gap will likely be closed after the first major LLM-driven cascade — the way most market structure improvements are made.

After.