The New York Stock Exchange has operated on a fixed schedule for most of its 230-year history.

Nine-thirty in the morning. Four in the afternoon. A defined window in which prices are discovered, orders are matched, and capital is deployed.

That schedule is ending.

Not with a single announcement. Not with a regulatory revolution. But with the quiet, persistent expansion of pre-market sessions, after-hours trading, overnight equity markets, and the structural pressure of a global investor base that does not stop caring about prices when New York goes to sleep.

The question for systematic traders is not whether markets will become 24-hour. That trajectory is clear. The question is what it means for strategies built around session boundaries, overnight gaps, and the rhythm of market open and close.

The Liquidity Illusion

The first thing most traders notice when they venture outside regular session hours is that they can still transact. Quotes exist. Prices move. Orders fill.

What is harder to see immediately is that the quality of that liquidity is fundamentally different.

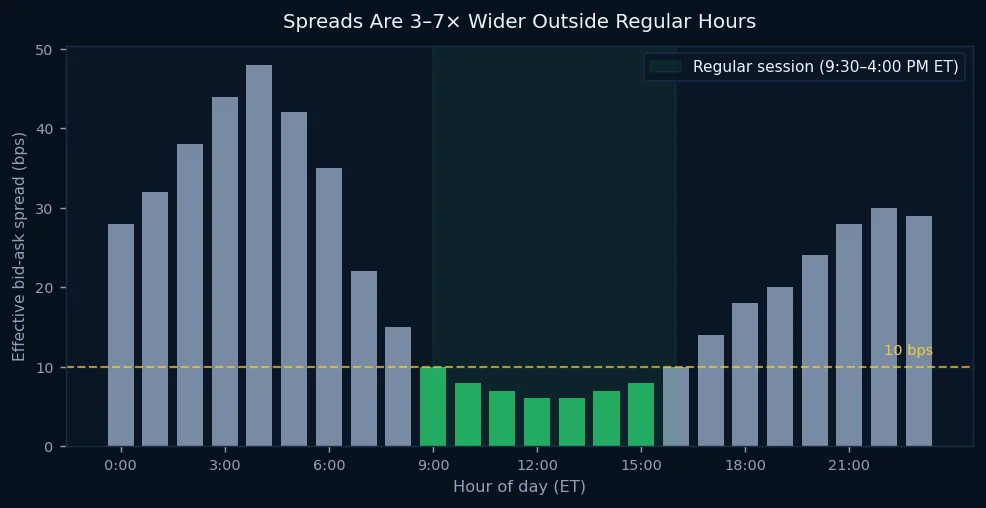

Bid-ask spreads in the overnight session are three to seven times wider than during regular hours, depending on the security. Volume is a fraction of the daytime flow. The market makers who compete aggressively to provide tight quotes from 9:30 to 4:00 are running reduced staffing or automated risk limits overnight.

This creates a trap for the unprepared. A trader who sees a quote and executes at 2:00 AM may receive a fill that looks reasonable. The spread they paid — hidden within the quoted price — may represent a transaction cost multiple times larger than they would have incurred at noon.

For retail traders reacting to overnight news, this asymmetry is systematically exploited. Institutional traders with direct market access and superior routing can often obtain better fills than individual investors facing the same quoted prices.

Volume Is Migrating

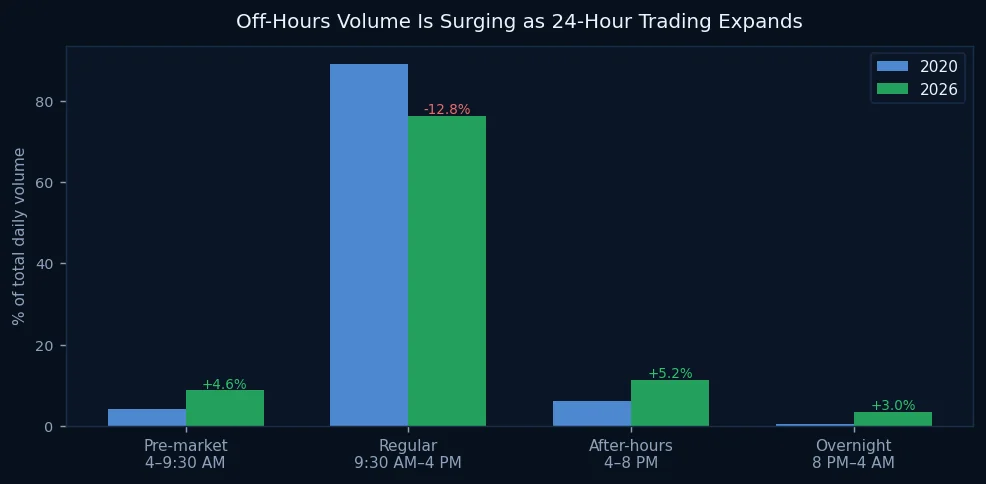

Despite the liquidity premium, off-hours trading is growing substantially.

The pre-market session has more than doubled its share of daily volume since 2020. After-hours trading has similarly expanded. Even the true overnight session — midnight to early morning — has gone from a statistical rounding error to a recognizable fraction of daily flow.

The drivers are structural: global retail participation, the crypto market's 24-hour precedent normalizing around-the-clock trading expectations, earnings announcements increasingly released outside market hours, and broker platforms making off-hours trading frictionless to execute.

This migration is not going to reverse. Once trading infrastructure extends to new hours, it tends to stay there. The NYSE's proposal to extend official trading hours to 22 hours per day is not a radical departure from trajectory — it is an acknowledgment of where liquidity is already heading.

The Gap Compression Problem

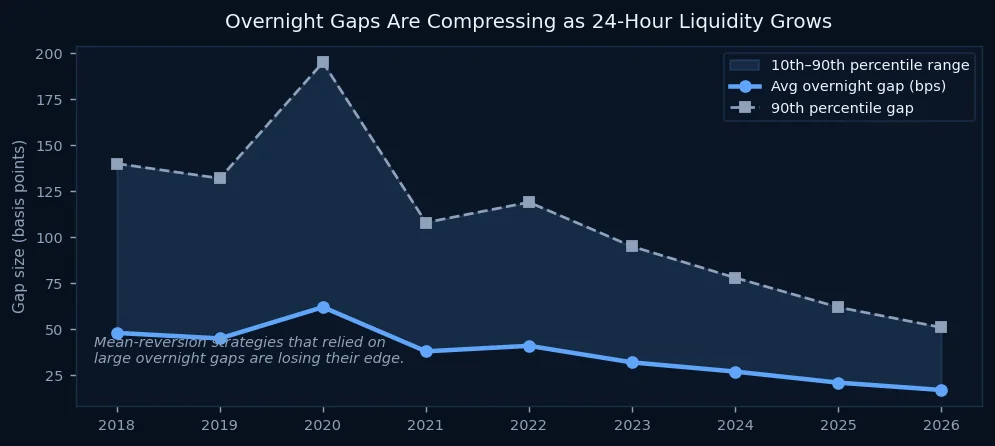

For a generation of systematic traders, the overnight gap was a feature, not a bug.

Strategies built around fading extended overnight moves, capturing gap fill patterns, or exploiting the repricing that occurred when New York opened after an Asian or European session had moved were consistent edge generators for years.

As overnight liquidity has improved, those gaps have compressed dramatically. The average overnight gap in S&P futures has fallen from roughly 48 basis points in 2018 to approximately 17 basis points today. The 90th percentile gap — the large moves that once created significant trading opportunities — has similarly compressed from 140 to 51 basis points.

The signal still exists. But the magnitude has declined substantially, and the competition for the remaining signal has intensified as more capital focuses on the same diminishing patterns.

What Systematic Traders Should Be Watching

The transition to extended hours creates both problems and opportunities for algorithmic systems.

The problems are clear: Strategies calibrated on regular session data — volatility estimates, correlation matrices, mean reversion parameters — may not transfer to extended session conditions. A system designed to trade the 10:00 AM to 2:00 PM window may misbehave if it fires a signal during the overnight session with dramatically different liquidity characteristics.

The opportunities are less obvious but real: As volume migrates, the price-setting process during regular hours is increasingly influenced by what happened overnight. The first thirty minutes of the regular session are increasingly a repricing of overnight moves rather than a fresh open. Systems that correctly model overnight positioning will have better context for predicting early session behavior.

The traders who will navigate this transition most effectively are those who treat session boundaries not as fixed rules, but as fluid parameters that describe the current liquidity environment — and adjust their signals accordingly.

The 24-hour market is not the future. For futures traders, it has always been the reality. For equity traders, it is becoming one.