There is a product sitting in millions of retail brokerage accounts that does not do what its name implies.

It says three times. It means something more complicated than that — and the difference between the expectation and the reality has quietly transferred billions of dollars from retail investors to market makers, arbitrageurs, and the brokers who facilitated the transaction.

The leveraged ETF. And specifically, the growing ecosystem of 3×, 5×, and now 10× products that have proliferated as retail appetite for amplified returns has expanded beyond what the traditional margin system could satisfy.

Understanding how these instruments actually work — and what role they play in daily market structure — is increasingly essential for anyone trading systematically in US equities.

The Daily Reset Problem

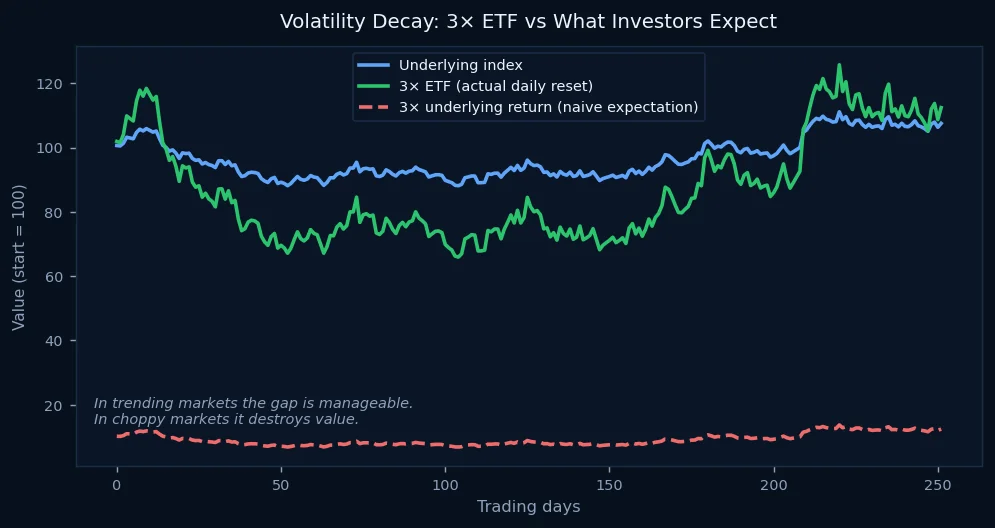

A leveraged ETF does not provide leveraged exposure to the underlying over time. It provides leveraged exposure each day, and then resets.

This is not a bug. It is the mathematical consequence of how these funds are structured. A 3× S&P 500 ETF guarantees that if the index rises 1% today, the fund rises approximately 3% today. It makes no guarantee about what happens over a week, a month, or a year.

The compounding problem emerges in volatile markets. If the index falls 10% and then rises 10%, a naive investor expects to be back where they started. They are not — they are at 99% of their starting value (−10%, then +10% of the lower base). Now apply 3× leverage: down 30%, then up 30%, you are at 91% of start. Do that for a year of choppy sideways action and the erosion is severe.

The technical term is volatility decay or beta slippage. It is not a fee. It is not manipulation. It is arithmetic.

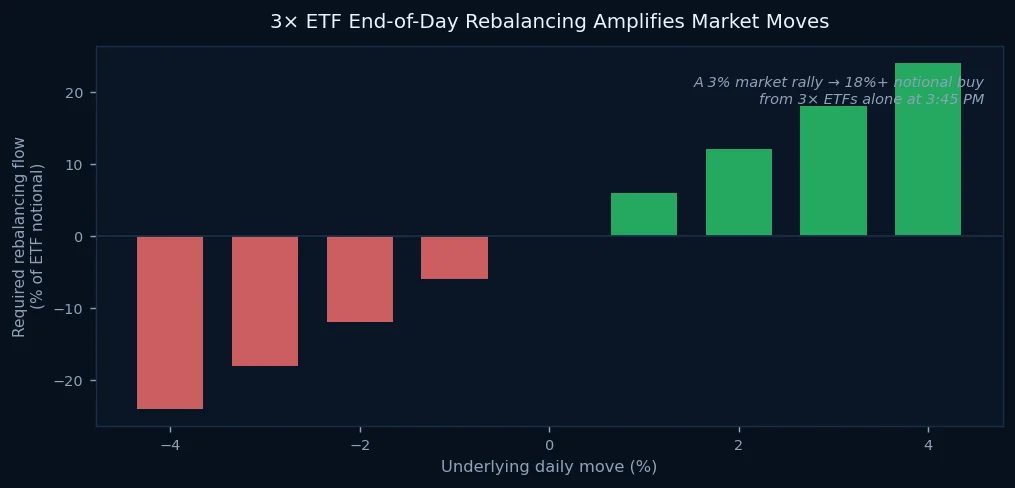

Why This Matters at 3:45 PM Every Day

There is a second effect that directly impacts active traders, even those who have never owned a leveraged ETF in their lives.

Because leveraged ETFs must rebalance daily to maintain their stated exposure, they generate large, predictable, directional orders near the market close.

On a day when the S&P rises 2%, 3× ETFs need to buy more exposure to maintain their leverage ratio. On a day when it falls 2%, they must sell. The size of these flows scales with the size of assets under management — and AUM in leveraged products has grown enormously.

The result: on strong directional days, the last thirty minutes see mechanically amplified flows in the same direction as the day's move. Trend-following algorithms that catch this dynamic have a structural advantage. Algorithms that fade the last-hour move into earnings are fighting against a mechanical freight train.

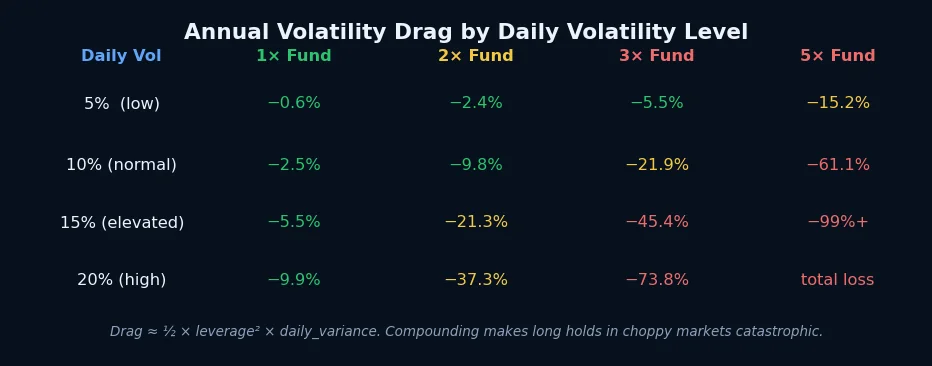

The Volatility Drag Table Nobody Shows You

The mathematics of volatility drag compound quickly. At typical equity market volatility — roughly 10% daily annualized — a 3× ETF loses approximately 22% per year to decay alone, before any directional loss. At elevated volatility of 15%, that figure approaches 45%.

This does not mean leveraged ETFs are useless. For short-term directional bets where a trader is actively managing exposure, they can be efficient instruments. The problem is how they are marketed, positioned, and held.

Most retail holders of TQQQ have not modeled volatility drag. They know the tech sector went up and they wanted three times of that. They are taking on a product whose long-term mechanics differ fundamentally from what the marketing implies.

The Edge on the Other Side

For systematic traders who understand these mechanics, the predictability creates opportunity.

The daily rebalancing flow is not random. Its size and direction can be estimated in real time based on the day's move and publicly available AUM data. The timing is constrained to the final hour of trading. The instruments affected — primarily S&P and Nasdaq futures — are among the most liquid in the world.

This does not mean the edge is unlimited or easy to capture. Sophisticated players compete for the same signal. Transaction costs matter. The flow estimate carries significant uncertainty.

But it is a real structural dynamic, built into the architecture of products that now manage hundreds of billions in assets.

The leveraged ETF was designed to amplify returns. It has also, as a side effect, amplified the predictability of certain market microstructure patterns — for those who know where to look.