For three years, one trade dominated everything.

Buy the companies building artificial intelligence infrastructure. Own the hyperscalers. Hold the chip makers. The logic was unassailable: AI was the defining technology of the decade, and the companies at the center of it would compound indefinitely.

It worked. Spectacularly. The Magnificent Seven stocks — Nvidia, Apple, Microsoft, Amazon, Alphabet, Meta, Tesla — generated returns that made everything else look like opportunity cost.

And then, quietly, without a single dramatic announcement, the trade began to reverse.

The Russell 2000 is up 18.3 percent year-to-date as of June 2026. The S&P 500 is up 8.9 percent.

That gap is not a rotation story. It is not a rate-cut story. It is not a recession signal.

It is something more interesting and more durable: a rational reappraisal of AI valuations by investors who have finally started asking what the earnings actually justify.

The Number That Doesn't Work

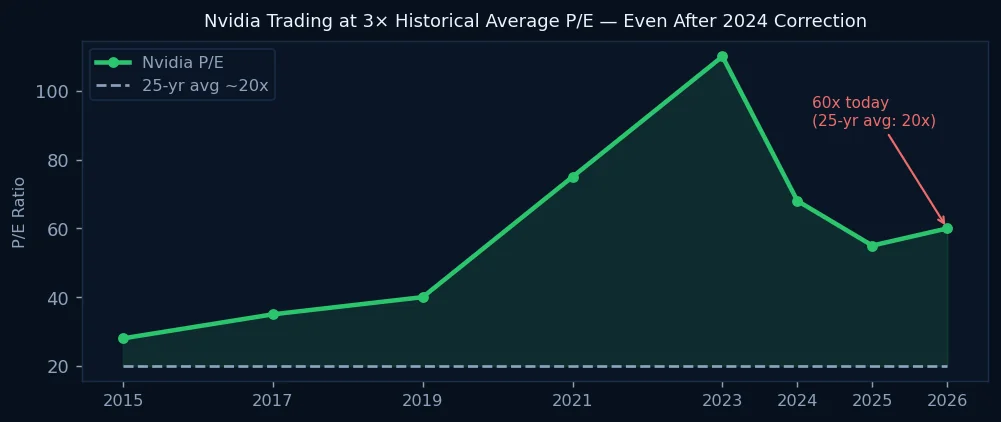

Start with Nvidia, because Nvidia is the purest expression of the AI trade.

The company is genuinely extraordinary. Its GPUs power the training infrastructure for virtually every significant AI model in production. Its competitive position in high-performance compute is real. Its revenue growth over the past three years has been among the most dramatic in the history of large-cap technology.

And it trades at sixty times earnings.

The twenty-five-year historical average price-to-earnings ratio for Nvidia is approximately twenty. The stock currently trades at three times that average.

This is not a gotcha. High-growth companies routinely trade at premiums to historical averages. The question is whether the premium is justified by the growth rate — and more specifically, whether the growth rate implied by a sixty-times earnings multiple can actually materialize.

Sustaining a sixty-times earnings multiple requires earnings to grow dramatically. If Nvidia's earnings grow fifty percent annually for five years — an extraordinary achievement for any company at any scale — the forward P/E still remains elevated relative to the broader market.

Institutional investors are not stupid. They can run this math. And an increasing number of them have concluded that at sixty times earnings, even the optimistic scenario does not justify the current price.

What the Rotation Actually Is

The conventional narrative about small-cap outperformance frames it as either a rate-cut play (smaller companies benefit more from cheaper borrowing) or a defensive rotation (investors moving to lower-beta assets ahead of a recession).

Both narratives are wrong, or at least incomplete.

The Federal Reserve has not cut rates. There is no rate-cut story operative here. Core inflation remains above target, and the June FOMC meeting produced no change in policy.

And recession indicators are not flashing. Employment remains strong. GDP growth, while moderating, is positive. Credit spreads have not widened to levels consistent with institutional recession positioning.

The rotation is not defensive. It is valuationally driven.

Institutional allocators with mandates to maintain certain return targets are doing straightforward math. A portfolio concentrated in stocks trading at twenty-five to sixty times earnings requires those earnings to materialize at scale. If any meaningful fraction of the AI earnings story disappoints — if data center buildout pauses, if enterprise AI adoption is slower than projected, if the next generation of chips faces supply constraints — the downside from these multiples is severe.

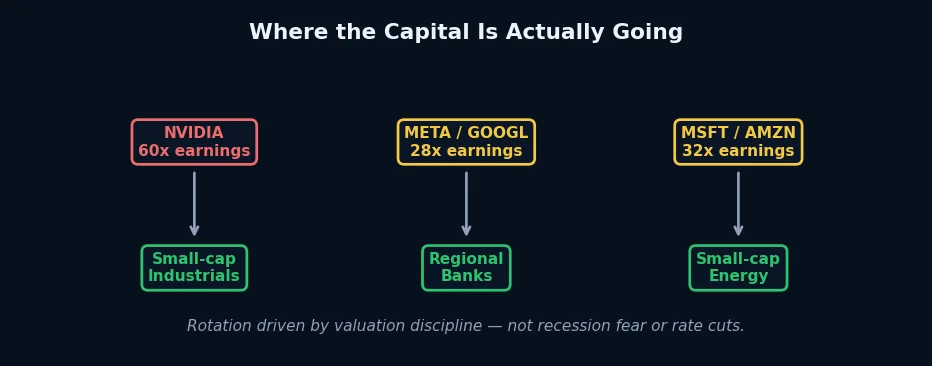

Small-cap industrials, regional banks, and small-cap energy companies trade at ten to fifteen times earnings. They do not require a revolutionary technology narrative to justify their prices. They simply need to continue generating the earnings they are already generating.

The capital moving from mega-cap AI into small-cap value is not pessimistic. It is rational reallocation by investors who have held AI exposure for three years, captured extraordinary gains, and are now asking a simple question: what is the probability that the next three years produce returns proportional to the current multiple?

The Timing Signal Worth Watching

Here is the complexity that makes this rotation fascinating rather than straightforward.

Small-cap outperformance will not continue indefinitely. At some point, Q2 and Q3 earnings from the AI infrastructure names will arrive. If those earnings beat expectations — and Nvidia in particular has a strong track record of exceeding consensus — the trade reverses. Capital flows back to mega-cap tech, the Russell 2000 underperforms, and the rotation narrative gets declared prematurely.

This is the typical pattern. Rotations into small-cap historically last between three and twelve months before AI or technology narratives reassert dominance. We are currently four months into this one.

The signal to watch is not the Russell 2000 level. It is the earnings revision trend for mega-cap AI names in Q2.

If Nvidia guides down — if Microsoft's Azure AI revenue misses — if the hyperscaler capex cycle produces returns below what the market has priced — the rotation deepens and extends. If earnings beat, the rotation ends quickly.

This creates an asymmetric setup. The rotation trade has already produced 18.3 percent. The downside from here — if AI earnings beat — is a return to mega-cap concentration. The upside — if AI earnings disappoint — is a continuation and deepening of the most significant valuation rebalancing in several years.

What This Means for Algo Traders

The Russell 2000 rotation has direct implications for strategies that operate in ES and NQ futures.

NQ futures — tracking the Nasdaq 100 — are dominated by the same mega-cap AI names that are being rotated out of. When institutional capital exits Nvidia and Microsoft into small-cap industrials, the NQ index experiences selling pressure even if the broader equity market is stable.

ES futures — tracking the S&P 500 — are more diversified but still heavily weighted to mega-cap technology. The top ten holdings of the S&P 500 represent nearly thirty-five percent of the index.

Strategies calibrated on the post-2020 regime — where mega-cap AI leadership translated directly into NQ strength and ES correlation — are operating in a different environment. The leadership has rotated. The instruments that historically led the equity market higher are now the source of relative underperformance.

This is not a trading recommendation. It is a structural observation: the correlation regime that governed NQ and ES performance for three years has shifted, and strategies that have not adapted to that shift are working against an inconvenient headwind.

The Deeper Question

The Russell 2000 rotation is, at its core, a story about what happens when a transformational technology narrative runs ahead of the underlying economics.

AI is real. The productivity gains are real. The infrastructure buildout is real. Nobody rational disputes any of that.

But real technology and correctly priced technology are different things. The internet was real in 1999. The smartphone was real in 2007. Both transformed civilization. Both also produced valuations that required a painful correction before the long-term trajectory reasserted itself.

The rotation happening now does not require AI to fail. It does not require Nvidia to miss earnings or Microsoft to announce a strategic retreat.

It only requires institutional capital to ask, quietly and methodically, whether sixty times earnings adequately compensates for the risk that the next three years might look different from the last three.

Increasingly, the answer is no.

And that answer is moving eighteen percent of capital into places that were not interesting two years ago.

That is not a crash. It is not a bubble bursting.

It is something more mundane and more important: price discovery, finally arriving.