There is a specific kind of market danger that does not look like danger until it is too late to do anything about it.

It does not announce itself with elevated volatility. It does not come with flashing warning signals or elevated credit spreads. It arrives quietly, in the form of suppressed numbers that feel comfortable — right up until the moment they are not.

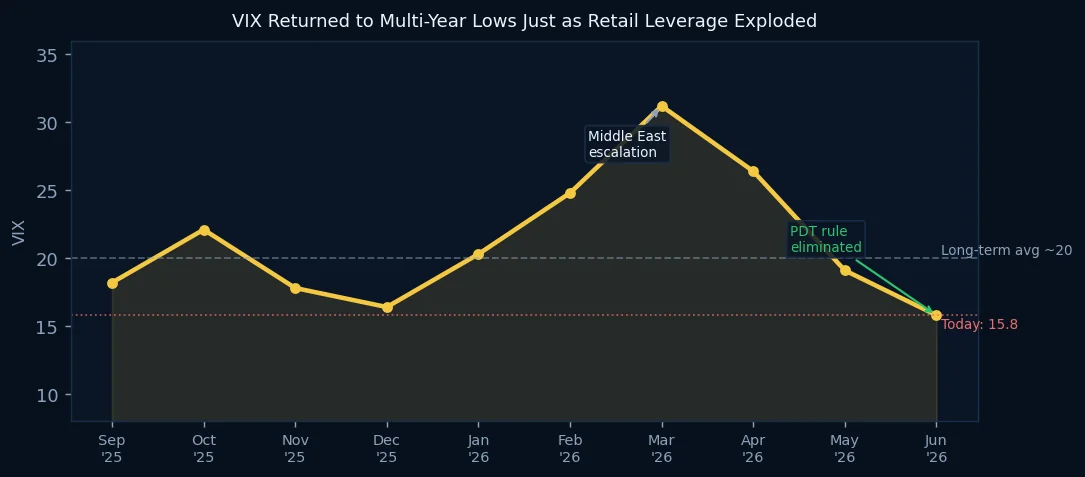

The VIX at 15.77.

On its face, this is a good number. It implies calm. It implies that professional investors — the people who set the price of risk — are not particularly worried. And in the short run, they may be right.

But calm has a cost. And right now, that cost is being hidden by one of the most consequential structural changes in retail market access in twenty years.

The Pattern Day Trader rule is gone.

And almost nobody has written about what happens when those two things occupy the same market at the same time.

The Mechanics of Suppressed Volatility

The VIX is not a mood indicator. It is derived from the prices of S&P 500 options — specifically, from what buyers and sellers of those options are willing to pay for protection against large moves.

When VIX is low, it means options are cheap. Which means selling options is attractive. Which means professional volatility sellers — market makers, hedge funds, systematic vol-selling strategies — are accumulating large short-gamma books.

Short gamma has a specific mechanical consequence: as the underlying moves, the position loses money faster and faster, requiring increasingly aggressive hedging.

When VIX is elevated, this dynamic is somewhat contained — sellers are fewer, positions are smaller, the market has already partially priced in the risk. When VIX is suppressed at fifteen-year lows, the dynamic is concentrated. Every vol seller has been rewarded for months. Books are large. And the market has become structurally dependent on continued calm to sustain those positions.

This is not speculation. This is the documented mechanics of what happened in February 2018 — the Volmageddon event — when the XIV volatility product collapsed fourteen percent in a single afternoon after years of quiet vol selling had accumulated into a self-reinforcing structure. The VIX that day tripled in hours.

The market rebuilt. It always does. But the holders of those short-gamma positions did not.

The PDT Change Nobody Has Quantified

On June 4, 2026, the twenty-five-year-old Pattern Day Trader rule was officially eliminated.

The $25,000 minimum account requirement for unrestricted day trading is gone. A trader with $2,000 can now execute unlimited same-day equity and options trades without restriction.

This is broadly covered as a democratization story. And it is. But the coverage has focused almost entirely on access — who can now trade that could not before.

The question nobody is asking is: what do newly unrestricted retail traders do first?

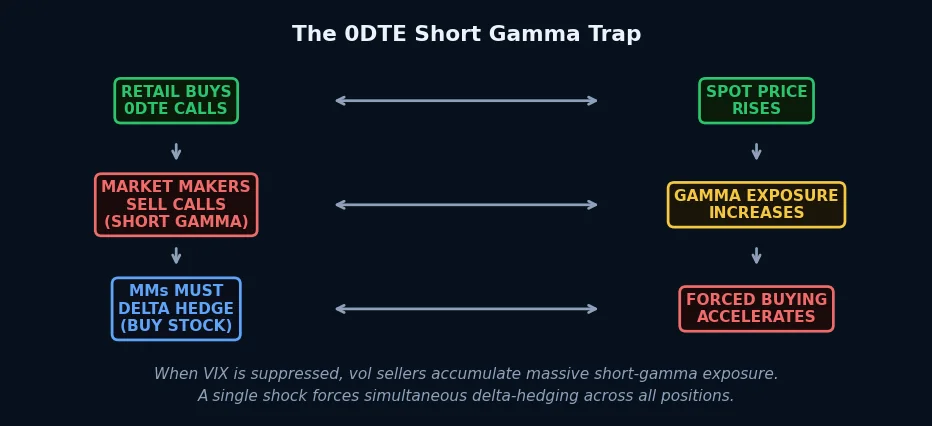

The answer, based on every observable pattern from the past five years of retail trading evolution, is options. Specifically, short-dated options. Specifically, zero-day-to-expiry options — 0DTE contracts that expire the same day they are traded.

0DTE options have grown from roughly five percent of S&P 500 options volume in 2020 to over forty-five percent by early 2026. They are the preferred instrument of retail coordination because they offer maximum leverage for minimum premium. A one-percent move in the underlying can produce a ten-to-one return on a well-timed 0DTE call.

They are also the instrument that most directly affects the gamma exposure of market makers.

When retail floods into 0DTE calls, market makers who sell those calls must continuously delta-hedge — buying the underlying as it rises, selling as it falls. This amplifies moves in both directions. The effect is most severe when call buying is concentrated and directional.

PDT elimination is about to produce a meaningful increase in the population of retail traders with both the access and the incentive to execute exactly this kind of coordinated, short-dated options activity.

The Convergence

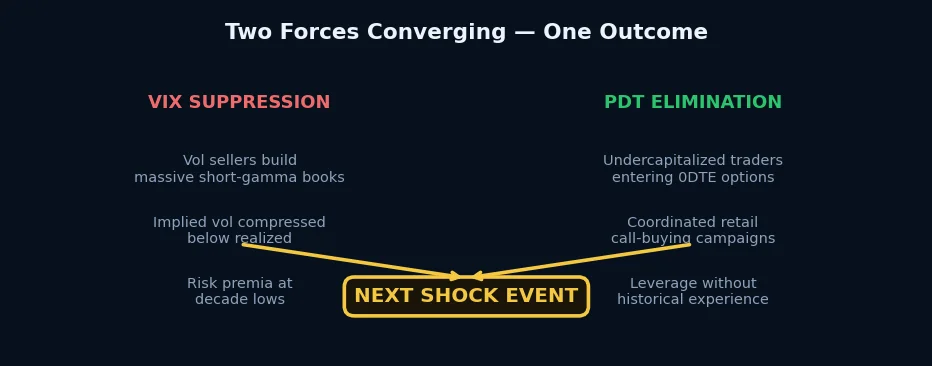

Two forces are now pointing at the same market structure simultaneously.

On one side: professional vol sellers with large short-gamma books, accumulated during a multi-month period of suppressed volatility. Their positions are profitable today. They will remain profitable in the absence of a shock. But their collective exposure to a sudden volatility spike is near historical highs.

On the other side: a newly expanded retail population with lower barriers to entry, a demonstrated preference for short-dated options, and coordination infrastructure — social platforms, trading communities, shared analytics — that did not exist during previous periods of VIX suppression.

The question is not whether these two forces will interact. They already are. The question is whether the interaction remains orderly or whether a catalyst — a geopolitical event, an earnings surprise, a Fed communication error — produces the kind of forced unwind that turns a normal correction into a volatility cascade.

What A Cascade Looks Like

The sequence is not complicated.

An external event causes a modest decline in the S&P 500 — say, two percent intraday. Under normal conditions, this is absorbed without systemic consequences. Buyers step in. Vol sellers adjust their hedges. The market finds equilibrium.

But if vol sellers are maximally exposed — if their short-gamma books are at scale consistent with months of VIX at fifteen — the delta-hedging requirement from a two-percent move is dramatically larger than it would have been during a period of elevated volatility. They must sell more to hedge. Selling drives price lower. Lower price triggers more hedging. The feedback loop self-reinforces.

Meanwhile, retail traders who have recently entered 0DTE positions — calls purchased in the morning on the assumption of continuation — watch their positions go to zero rapidly. Stop-losses trigger. Margin calls hit accounts that do not have the capital cushion to absorb a sudden move.

The dynamic is not identical to 2018. The instruments are different, the participants are different, and the market structure has evolved. But the underlying logic — concentrated short-gamma exposure meeting an unexpected move — is structurally similar.

The Asymmetry

The frustrating truth about this setup is that it may never resolve dramatically. Markets can sustain uncomfortable structural positions for much longer than rational analysis suggests. VIX at fifteen does not mean a crash is imminent. It may stay at fifteen or lower for months.

But the asymmetry of the risk is worth understanding clearly.

If nothing happens: vol sellers collect premium, retail traders make money on their 0DTE calls, the VIX stays suppressed, and this analysis looks wrong.

If something happens: the combination of maximum short-gamma exposure and a newly leveraged retail population creates a feedback loop that turns a two-percent correction into something that looks much more disorderly.

The expected value calculation is not about probability of crash. It is about the consequence of being wrong on the downside in a market where the structural cushion has been deliberately removed.

Low volatility is not safety. Sometimes it is the precondition for the opposite.

The VIX at fifteen is not a signal to panic. But it is a signal to understand exactly what is underneath the calm — and to position accordingly before the moment when everyone else wants to do the same thing at the same time.