On February 28, 2026, markets entered a new regime.

It happened with the speed that geopolitical events typically move when they finally arrive: faster than models expected, in a direction that most portfolios were not positioned for, and with consequences that are still unfolding.

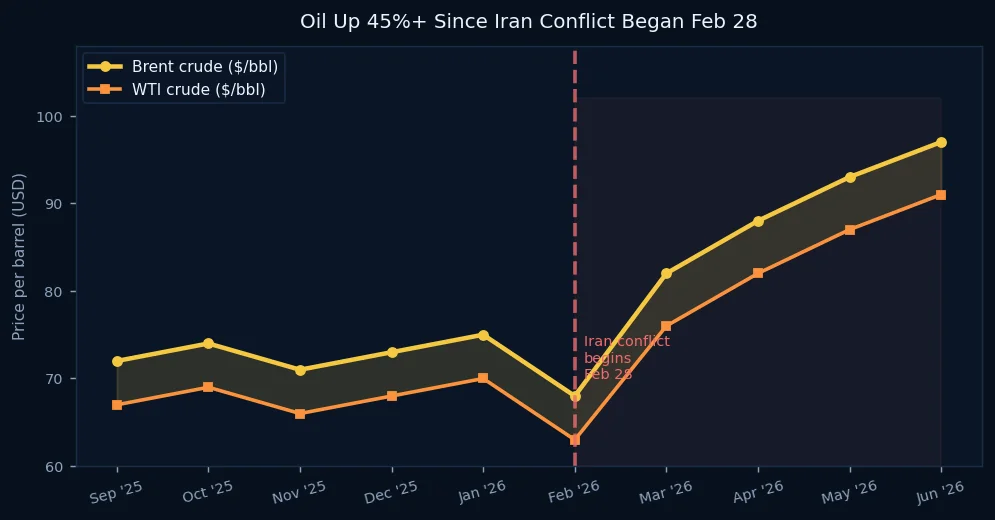

The Iran conflict and the subsequent partial closure of the Strait of Hormuz — through which approximately 20% of the world's traded oil passes — triggered a supply shock that has sent Brent crude from below $70 to above $97 per barrel.

For systematic traders running strategies calibrated on the market conditions of 2024 and 2025, this represents something more significant than a move in one commodity. It represents a regime change — a structural shift in how asset classes relate to each other, which variables drive returns, and which historical patterns remain valid.

The Oil Spike by the Numbers

Brent crude has risen more than 45% since the conflict began. Fourteen million barrels per day of Middle Eastern supply were disrupted in the initial phase, with refined product shortages cascading through the distribution network over weeks.

The consensus forecast among major banks now centers on Brent averaging the low-to-mid $90s through year-end, with credible upside to $100 if the Strait of Hormuz situation does not meaningfully improve. The pre-conflict estimate, from February 2026, was roughly $68.

That is a 40% revision in the course of four months. For any model that treated oil as a mean-reverting variable within a stable band — as many did — that revision represents a systematic forecasting failure.

The Correlation Problem

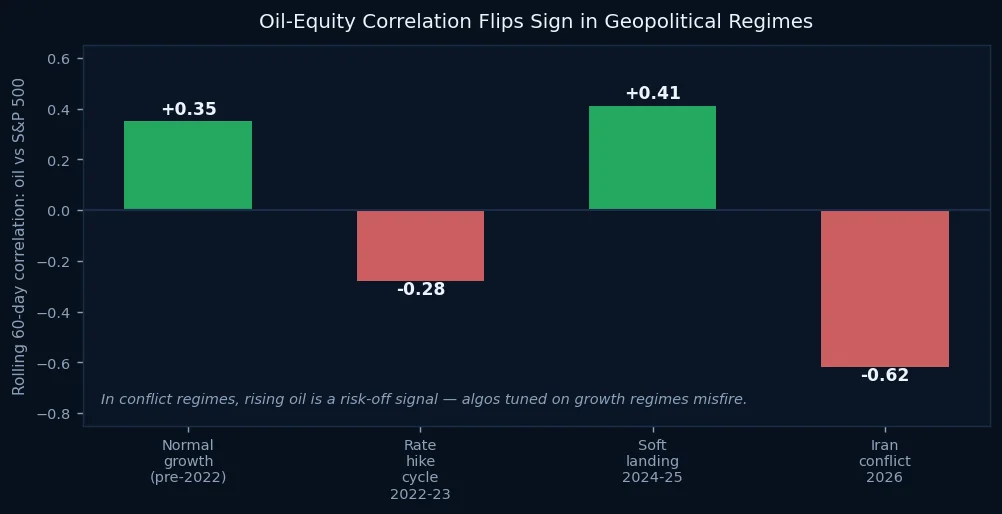

What makes geopolitical regime shifts particularly dangerous for algorithmic systems is that they do not merely change the level of prices. They change the relationships between prices.

In a normal growth regime, oil and equities tend to move together — both reflecting economic expansion. When growth is strong, demand for oil rises and corporate earnings improve simultaneously.

In a geopolitical supply shock, the relationship inverts. Rising oil prices are inflationary and margin-compressive. They act as a tax on economic activity. Consumers spend more at the pump and less elsewhere. Corporate input costs rise. Central banks face the impossible choice between fighting inflation and supporting growth.

In the current regime, the rolling correlation between oil prices and the S&P 500 has turned sharply negative at −0.62. A strategy that used oil's direction as a confirming signal for equity momentum — reasonable in 2024 — is now systematically misfiring.

The Sector Divergence

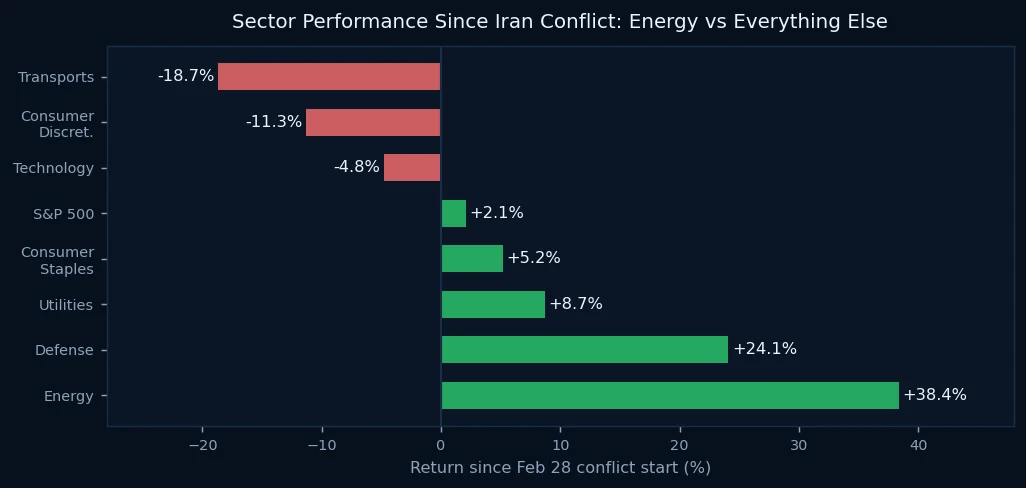

The sectoral consequences have been dramatic. Energy is up 38% since February 28. Defense, benefiting from elevated geopolitical spending, is up 24%. Utilities and consumer staples — traditional safe havens — are modestly positive.

Technology is negative. Consumer discretionary is down double digits. Transports, crushed by fuel costs, have lost nearly 19%.

For a long-only momentum system that entered the year with a technology-heavy portfolio — entirely rational given 2024's performance — the regime shift has been painful in ways that aggregate index returns obscure. The S&P 500 is up approximately 2% since the conflict. But that aggregate masks a massive internal rotation that most index-benchmarked strategies failed to navigate.

What Regime-Aware Trading Actually Means

The phrase "regime-aware" appears frequently in systematic trading marketing. Most of what is marketed under that label is not actually regime-aware — it is lag-aware. The model detects that something has changed after the fact and adjusts. By then, the damage is done.

Genuine regime awareness requires a different approach: models that explicitly track the structural drivers of market behavior — not just price and volume, but the underlying economic and geopolitical forces that determine how assets relate to each other.

In the current environment, those drivers include: - Strait of Hormuz throughput as a real-time supply signal - US-Iran diplomatic communications as a forward-looking regime indicator - Refinery crack spreads as a measure of downstream supply stress - Treasury inflation breakevens as the market's own regime assessment

None of these are exotic. All are publicly available. What distinguishes traders who navigate regime shifts from those who don't is not the possession of better data — it is the willingness to monitor variables that fall outside the comfortable historical patterns on which most strategies were built.

The market that existed in 2025 is not the market that exists today. The algorithms that worked in 2025 need to know that.