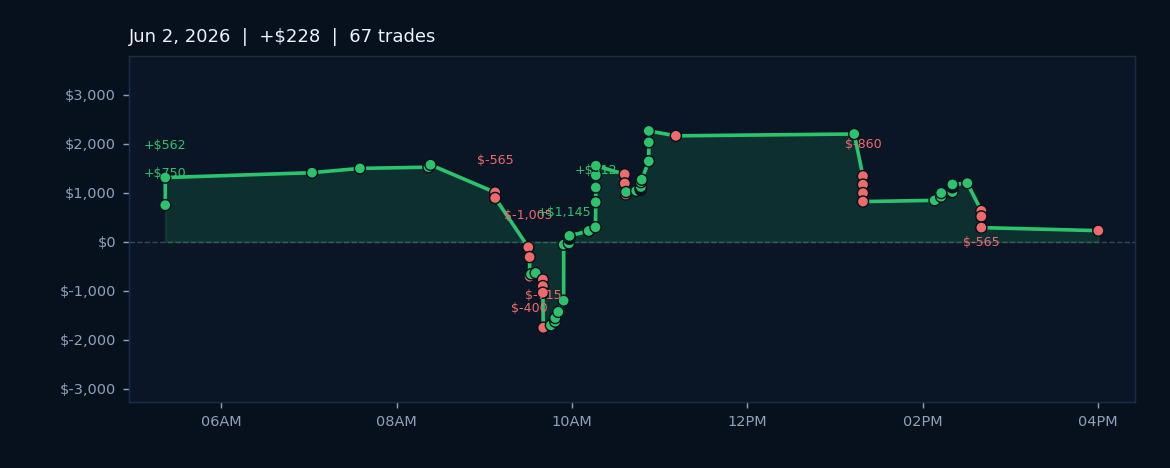

The algos operated in a trend regime today with 59.5% probability weighting, capitalizing on directional conviction to post $228.50 net P&L across 67 trades and a respectable 68.7% win rate. Market sentiment registered positive across the AI panel, providing structural support for long positioning in ES and NQ futures throughout the session. The execution quality remained steady, though the day underscores an increasingly important operational insight: not all trading hours are created equal.

The morning window proved most productive, with our flagship ES contract strategy generating $4,140 net P&L during the 8:00 AM ET hour and $2,390 in the 9:00 AM slot, averaging $108.95 and $88.52 per trade respectively. This concentration of edge in early North American hours has triggered an active recommendation to cease trading after 9:00 AM ET on this strategy, as subsequent hours have shown materially weaker risk-reward dynamics. Separately, the midday 12:00 to 14:00 ET window in our NQ strategy continues to drag performance, with the noon hour alone responsible for negative $1,265 across 17 trades.

A broader caution flag has emerged: the most recent 30 trades on the NQ strategy show a profit factor of only 1.07 and a win rate that has compressed to 53.3% from an overall baseline of 65.5%, signaling potential regime degradation or parameter drift that warrants attention. Concurrently, Monday trading remains flagged as catastrophically unprofitable across our sample set, averaging negative $211.38 per trade. With ADP employment and ISM Services data due tomorrow and AVGO earnings on the calendar for Wednesday, the algos are positioned to stay alert for volatility inflection points that may reset intraday patterns.